ISACA Cincinnati Chapter March Meeting

|

|

|

- Avice Reynolds

- 5 years ago

- Views:

Transcription

1 ISACA Cincinnati Chapter March Meeting Recent and Proposed Changes to SOC Reports Impacting Service and User Organizations. March 3, 2015 Presenters: Sayontan Basu-Mallick Lori Johnson

2 Agenda SOCR Overview Difference between SOC1, SOC2 and SOC3 Changing SOCR Community Update to ISAE 3402 Changes to the AICPA attestation standards SOC 2 Trust Principal Update SOC 2 Plus Updates from an user organization perspective Independence Page 1

3 SOCR Overview

4 SOC 1 elements System People Processes Applications Infrastructure User entities financial statement assertions Risk assessment Controls System description Services provided Procedures Accounting records Significant events Entity-level controls Reporting User control considerations Control objectives Reasonable basis for management asserting controls were consistently applied Existing testing/ validation On-going monitoring Limited additional testing Management s written assertion Service auditor s report Page 3

5 SOC 1, SOC 2 or SOC 3? Other Page 4

6 SOC 1, SOC 2 or SOC 3? Who will use the communication? User s areas of interest? User s business Purpose? What criteria will the report measure against? Conclude on report type and distribution method? Direct consumer User entity Business Partner Management/ BOD User service organization Regulator Other Controls relevant to financial audits Security Availability Processing integrity Confidentiality Regulatory/ self regulatory Contractual compliance Meet audit needs Governance/ risk management Vendor management Regulatory compliance Contractual compliance Internal report management confidence Enhance trust regarding service Financial statement assertions Industry standards Contractually specified Regulatory requirements Other SOC 1 SOC 2 SOC 3 Agreed upon procedures AT 101, AT 601 Findings and recommendations (internal-use, no assurance provided) Privacy Other Other Page 5

7 SOC 2 and SOC 3 SOC 2 - Provides information about internal control at the service organization related to the Trust Services Principles - security, availability, processing integrity, confidentiality, or privacy (restricted use) SOC 3 - Provides information about the service organization s achievement of the Trust Services criteria related to security, availability, processing integrity, confidentiality, or privacy (general use) Page 6

8 A Service Provider Perspective Source: 2014 EY Service Organization Controls Reporting Survey Results Page 7

9 Changing SOCR Community

10 We are in the midst of significant changes for SOCR Alerts, changes, and guidance PCAOB Staff Audit Practice Alert #11 Timeline October 2013 (published) ISAE 3402 international guidance update December 15, 2015 (effective date) AT 801 US guidance update Updated Trust Services Principles and Criteria December 2015 or later (anticipated effective date) December 15, 2014 (effective date) Page 9

11 Changing Standards and Guidance New and Pending Guidance PCAOB Staff Audit Practice Alert No. 11 SOC 2 Guide Winter 2014 SOC 3 Guide Winter 2014/2015 Revised AICPA attestation standards, including AT Trust Services Privacy currently under revision Exposure provided in June 2014 Effective 2015 Page 10

12 PCAOB SAPA 11 observations other observations While the PCAOB has not directly focused on the quality of SOC 1 reports, many reports may not be deemed sufficient if subject to the scrutiny given to other audit documentation. Alert 11 identifies areas for specific improvement. Roll-forward of controls Obtain sufficient evidence to update the results of testing of controls from an interim date to year-end Using the work of others Sufficiently perform procedures regarding the use of the work of others Evaluating control deficiencies If a deviation exists and we conclude a control is not effective, do the remaining controls address the identified risks? Sufficiently evaluate identified control deficiencies Page 11

13 Update to ISAE 3402

14 Update to ISAE 3402 Updated ISAE3000 and ISAE3402 Released in December effective for reports dated on or after 15 December 2015 Most changes are technical reporting matters that will not be visible to the service provider ISAE3402 now a supplement to ISAE 3000 rather than a stand-alone standard Management s Assertion now Management s Statement Requirement that the service auditor s report contain a statement that the service auditor applies ISQC (International Standard on Quality Control) 1 Requirement that that the service auditor s report contain a statement that the service auditor complies with independence and other IESBA (International Ethics Standards Board for Accountants) code requirements Page 13

15 Significant changes (continued) Concept of engagement partner introduced Where required, has the appropriate authority from a professional, legal or regulatory body Engagement quality control review Risk-based approach Page 14

16 Changes to the AICPA attestation standards

17 Proposed changes to the AICPA attestation standards, including SOC 1 The AICPA Attestation Standards (published in the Statements on Standards for Attestation engagements or SSAEs) establish requirements for examining, reviewing, and applying agreedupon procedures to subject matter other than financial statements The Auditing Standards Board (ASB) is undertaking significant effort to improve the clarity and quality of the attestation standards The revised standards are expected to be finalized during the 4 th quarter 2015 Anticipated effective date is reports with an opinion date on or after May 1, 2017 Page 16

18 Summary of key changes for SOC 1 (AT 801) Changes to description Inclusion of complementary subservice organization controls when carve-out method is used Disclosure of monitoring controls over subservice organizations Sufficiency of descriptions of controls Descriptions of reports Definition of subservice organization still being discussed Definition of complementary user entity controls still being discussed Page 17

19 Summary of key changes for SOC 1 (continued) Changes in auditor responsibilities Clarifying the use of a risk-based approach to the service auditor s examination Understanding the internal audit function and reading all relevant reports Identification of the risk of material misstatement and evaluation of whether the description meets the needs of user auditors Evaluating control objectives and performing separate identification of the risks that threaten the achievement of the control objectives Excessive use of the work of internal audit still being discussed Page 18

20 Changes to the attestation standards Many similarities with revisions to ISAE 3000 Engagement partner Engagement risk-based approach Engagement quality control review Intended to be self-contained minimal reference to US auditing standards Page 19

21 Subservice organization challenge ISA 402/AU-C 402 If the user auditor plans to use a type 1 or a type 2 report that excludes the services provided by a subservice organization and those services are relevant to the audit of the user entity s financial statements, the user auditor shall apply the requirements of this ISA with respect to the services provided by the subservice organization. PCAOB inspections have identified failure to perform procedures on carved-out subservice organizations as an issue. User auditors are expressing greater concern over carved-out subservice organizations. Page 20

22 Subservice organizations - Issues in inclusive and carved-out reports Inclusive reports Subservice organizations are often reluctant to participate Provide services to multiple primary service organizations Contractual concerns Coordination of testing Carve-out reports No contractual relationship between users and subservice organization Report period Timing of report availability User organizations can monitor primary service providers, usually cannot monitor subservice organizations Users need to tie the subservice organization CUECs to controls at the primary service organization Page 21

23 Analysis of monitoring Understand user-entity financial statement assertions Identify control objectives Identify risks that threaten the achievement of the control objectives Identify the risks that are directly addressed by controls at the subservice organization Identify monitoring/reporting and other evidence that the controls at the subservice organization are functioning as designed Consider testing Page 22

24 Subservice organizations Resolving issues SOC 1 guide encourages description of monitoring controls even when carving-out Monitoring may be sufficient to make controls at vendor not relevant to users Examples of effective monitoring controls: Colocation Facility Controls: Physical access and environment Monitoring controls: physical access approvals, periodic evaluations Securities Pricing Services Controls: Valuation of investments Monitoring controls: Pricing comparison Page 23

25 Carved-out subservice organization CUECs Identifies risks that threaten the achievement of the control objectives Includes risks that arise from using a subservice organization Usually will include risk that subservice organization CUECs need to address If a SOC 1 report is not available from the subservice organization, consider manuals, contracts or other communications from the subservice organization Page 24

26 SOC2 Trust Principal Update

27 SOC reporting trends Current State Which of the following areas are seeing an increased interest / demand for independent assurance from your clients? Processes not related to financial transaction (e.g., customer management) 20% Regulatory Compliance (e.g., Financial Market Supervisory Authority) 67% Cloud Services 22% SOC2 Elements Data Integrity 59% Availability / business continuity 71% Data Privacy 59% Source: 2014 EY Service Organization Controls Reporting Survey Results Page 26

28 The 2014 Trust Services principles and criteria Issued January 2014 Effective for periods ending on or after December 15, 2014, but early adoption encouraged Established by the Assurance Services Executive Committee (ASEC) of the AICPA Consolidates the common criteria across the Trust Services principles, security, availability, processing integrity, and confidentiality Page 27

29 The 2014 Trust Services principles and criteria SOC 2 principles and criteria PRINCIPLES CRITERIA Organization Communications Risk management Monitoring Access controls System operations Change Management Security Availability Processing Integrity Confidentiality X X X X X X X X X X X X X X X X X X X X X X X X X X X X Page 28

30 The 2014 Trust Services principles and criteria principles Established by the Assurance Services Executive Committee (ASEC) of the AICPA: Security: The system is protected against unauthorized access, use, or modification. Availability: The system is available for operation and use as committed or agreed. Processing integrity: System processing is complete, valid, accurate, timely, and authorized. Confidentiality: Information designated as confidential is protected as committed or agreed; Privacy: Addresses the system s collection, use, retention, disclosure, and disposal of personal information Page 29

31 SOC 2 expected 2015 changes Updated for 2014 Trust Service criteria Increased guidance to service auditors on how to plan and perform an engagement Sufficiency of description Suitability of design of controls Guidance by trust services grouping Principle Controls that did not operate during the period User entity responsibilities vs. complementary user entity controls Subservice organizations Page 30

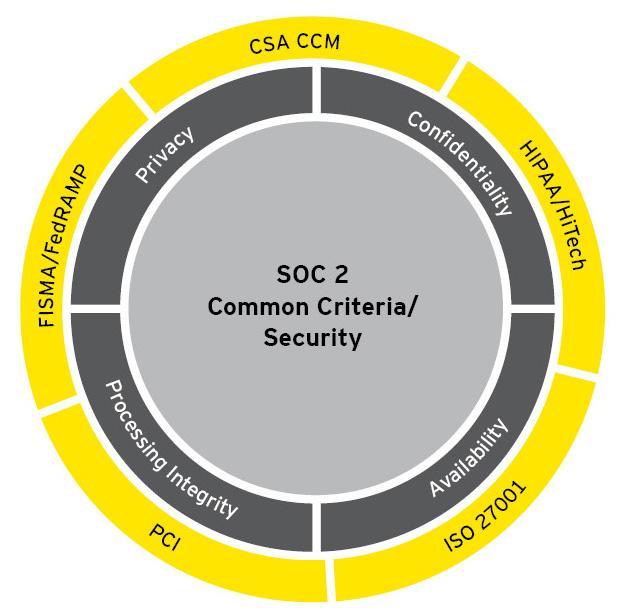

32 New SOC 2 reporting opportunities SOC 2 reporting options Report Level of effort Opinion SOC 2 Baseline Standard opinion SOC 2 with a mapping to another framework SOC 2 Plus Not likely to require additional controls outside of Trust Services Principles Controls required to align to Trust Services Principles and the selected framework(s) Standard opinion Standard opinion plus an opinion on the selected framework(s) Page 31

33 New SOC 2 reporting opportunities (continued) Common frameworks requested by our clients and their stakeholders: Framework Mapping to SOC 2 available SOC 2 Plus possible Other Attestation report ISO ISO Certification Cyber Security for Critical Infrastructure 4 4 NIST R4 In progress HIPAA 4 4 PCI 4 Cloud Security Alliance Cloud Control Matrix 4 4 FISMA Federal Risk and Authorization Management Program (FedRAMP) AT101 AT101 in progress Page 32

34 Multi-framework SOC2 Reporting

35 Updates from an user organization perspective

36 A User Organization Perspective Source: 2014 EY Service Organization Controls Reporting Survey Results Page 35

37 A User Organization Perspective (5) User auditor viewpoint on SOC report AICPA SOC 1 Guide 3.40 states that The degree of detail included in the description (SOC 1) generally is equivalent to the degree of detail a user auditor would need if the user entity were performing the outsourced services themselves This applies to all aspects of the SOC 1 report Auditor opinion Management assertion Description Evaluation of Carved out sub service providers Identified deficiencies Wording of controls Wording and results of testing Page 36

38 A User Organization Perspective (6) User auditor viewpoint on SOC report The description should be documented as if the user entity were performing the outsourced service Clear description of the process flow consider a flowchart Identification of key process owners, inputs, outputs, reports Control objectives related to financial statement and IT risks Description of relationship with carved out subservice providers, including the affected control objectives Increased level of detail provided in the test procedures and results section When describing controls Of the auditor s tests and results Identified deviations Page 37

39 Recent changes/trends that impact user organizations and user auditors Sufficiency of coverage provided by the Type 2 SOC report The PCAOB is increasingly questioning reliance on SOC reports when the SOC report does not cover an adequate period of the company s audit period. Adequacy is determined based on period covered in the SOC report, the nature of services provided, the risk of impacted accounts at the user organization, among other factors. Use of SOC 2 reports in support of financial statement audit This is becoming more acceptable where transaction processing and reporting services are not performed and the system description and controls can be adequately represented in a SOC 2 report. Page 38

40 Independence update

41 Independence update SEC matters Reports included in SEC filings or prepared to meet an SEC requirement (e.g., custody rule) bookkeeping services has been interpreted to include word processing and printing services and are prohibited Single user reports SEC has taken the position that a EY audit client user entity should not use an EY prepared single user SOC 1 report as it s basis for SOx assessment. Page 40

42 Questions?

43 EY Assurance Tax Transactions Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US Ernst & Young LLP. All Rights Reserved ED None This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice. ey.com

Evaluating SOC Reports and NEW Reporting Requirements

Evaluating SOC Reports and NEW Reporting Requirements ISACA Kris Lonborg, EY Partner Maria Avedissian, EY Senior Manager September 12, 2013 Agenda Evaluating SOC reports Recent changes made to the SOC1

Evaluating SOC Reports and NEW Reporting Requirements ISACA Kris Lonborg, EY Partner Maria Avedissian, EY Senior Manager September 12, 2013 Agenda Evaluating SOC reports Recent changes made to the SOC1

Retirement of SAS 70 and a new generation of Service Organization Control (SOC) Reports

Reports") new generation of Service Organization Control (SOC) Reports Presented by: Nina Currigan, KPMG Advisory Manager Karen Krebsbach, Ernst & Young Advisory Manager With you today Nina Currigan Advisory Manager

new generation of Service Organization Control (SOC) Reports Presented by: Nina Currigan, KPMG Advisory Manager Karen Krebsbach, Ernst & Young Advisory Manager With you today Nina Currigan Advisory Manager

SOC Reporting / SSAE 18 Update July, 2017

SOC Reporting / SSAE 18 Update July, 2017 Agenda SOC Refresher Overview of SSAE 18 Changes to SOC 1 Changes to SOC 2 Quiz / Questions Various Types of SOC Reports SOC for Service Organizations (http://www.aicpa.org/soc4so)

SOC Reporting / SSAE 18 Update July, 2017 Agenda SOC Refresher Overview of SSAE 18 Changes to SOC 1 Changes to SOC 2 Quiz / Questions Various Types of SOC Reports SOC for Service Organizations (http://www.aicpa.org/soc4so)

C22: SAS 70 Practices and Developments Todd Bishop, PricewaterhouseCoopers

C22: SAS 70 Practices and Developments Todd Bishop, PricewaterhouseCoopers SAS No. 70 Practices & Developments Todd Bishop Director, Risk Assurance Services, PricewaterhouseCoopers Agenda SAS 70 Background

C22: SAS 70 Practices and Developments Todd Bishop, PricewaterhouseCoopers SAS No. 70 Practices & Developments Todd Bishop Director, Risk Assurance Services, PricewaterhouseCoopers Agenda SAS 70 Background

Service Organization Control (SOC) Reports: What they are and what to do with them MARCH 21, 2017

Reports: What they are and what to do with them MARCH 21, 2017") Service Organization Control (SOC) Reports: What they are and what to do with them MARCH 21, 2017 Presenter Colin Wallace, CPA/CFF, CFE, CIA, CISA Partner Colin has provided management consulting and internal

Service Organization Control (SOC) Reports: What they are and what to do with them MARCH 21, 2017 Presenter Colin Wallace, CPA/CFF, CFE, CIA, CISA Partner Colin has provided management consulting and internal

Demonstrating data privacy for GDPR and beyond

Demonstrating data privacy for GDPR and beyond EY data privacy assurance services Introduction The General Data Protection Regulation (GDPR) is ushering in a new era of data privacy in Europe. Organizations

Demonstrating data privacy for GDPR and beyond EY data privacy assurance services Introduction The General Data Protection Regulation (GDPR) is ushering in a new era of data privacy in Europe. Organizations

PREPARING FOR SOC CHANGES. AN ARMANINO WHITE PAPER By Liam Collins, Partner-In-Charge, SOC Audit Practice

PREPARING FOR SOC CHANGES AN ARMANINO WHITE PAPER By Liam Collins, Partner-In-Charge, SOC Audit Practice On May 1, 2017, SSAE 18 went into effect and superseded SSAE 16. The following information is here

PREPARING FOR SOC CHANGES AN ARMANINO WHITE PAPER By Liam Collins, Partner-In-Charge, SOC Audit Practice On May 1, 2017, SSAE 18 went into effect and superseded SSAE 16. The following information is here

EY s data privacy service offering

EY s data privacy service offering How to transform your data privacy capabilities for an EU General Data Protection Regulation (GDPR) world Introduction Data privacy encompasses the rights and obligations

EY s data privacy service offering How to transform your data privacy capabilities for an EU General Data Protection Regulation (GDPR) world Introduction Data privacy encompasses the rights and obligations

SOC 2 examinations and SOC for Cybersecurity examinations: Understanding the key distinctions

SOC 2 examinations and SOC for Cybersecurity examinations: Understanding the key distinctions DISCLAIMER: The contents of this publication do not necessarily reflect the position or opinion of the American

SOC 2 examinations and SOC for Cybersecurity examinations: Understanding the key distinctions DISCLAIMER: The contents of this publication do not necessarily reflect the position or opinion of the American

SAS 70 & SSAE 16: Changes & Impact on Credit Unions. Agenda

SAS 70 & SSAE 16: Changes & Impact on Credit Unions John Mason CISM, CISA, CGEIT, CFE SingerLewak LLP October 19, 2010 Agenda Statement on Auditing Standards (SAS) 70 background Background & purpose Types

SAS 70 & SSAE 16: Changes & Impact on Credit Unions John Mason CISM, CISA, CGEIT, CFE SingerLewak LLP October 19, 2010 Agenda Statement on Auditing Standards (SAS) 70 background Background & purpose Types

Making trust evident Reporting on controls at Service Organizations

www.pwc.com Making trust evident Reporting on controls at Service Organizations 1 Does this picture look familiar to you? User Entity A User Entity B User Entity C Introduction and background Many entities

www.pwc.com Making trust evident Reporting on controls at Service Organizations 1 Does this picture look familiar to you? User Entity A User Entity B User Entity C Introduction and background Many entities

Adopting SSAE 18 for SOC 1 reports

Adopting SSAE 18 for SOC 1 reports Overview Since its adoption in 2011, service auditor reports issued in accordance with SSAE 16 have become increasingly common in the marketplace. In April 2016, the

Adopting SSAE 18 for SOC 1 reports Overview Since its adoption in 2011, service auditor reports issued in accordance with SSAE 16 have become increasingly common in the marketplace. In April 2016, the

Transitioning from SAS 70 to SSAE 16

Industry Webinar Series SAS 70 ENDS EXIT TO SSAE 16 Transitioning from SAS 70 to SSAE 16 How Does This Apply to Your Organization? Cindy Boyle, Partner Rodney Walsh, Director BKD IT Risk Services Agenda

Industry Webinar Series SAS 70 ENDS EXIT TO SSAE 16 Transitioning from SAS 70 to SSAE 16 How Does This Apply to Your Organization? Cindy Boyle, Partner Rodney Walsh, Director BKD IT Risk Services Agenda

SAS 70 SOC 1 SOC 2 SOC 3. Type 1 Type 2

SAAABA Changes in Reports on Service Organization Controls April 18, 2012 Changes in Reports on Service Organization Controls (formerly SAS 70) April 18, 2012 Duane M. Reyhl, CPA Andrews Hooper Pavlik

SAAABA Changes in Reports on Service Organization Controls April 18, 2012 Changes in Reports on Service Organization Controls (formerly SAS 70) April 18, 2012 Duane M. Reyhl, CPA Andrews Hooper Pavlik

SOC for cybersecurity

April 2018 SOC for cybersecurity a backgrounder Acknowledgments Special thanks to Francette Bueno, Senior Manager, Advisory Services, Ernst & Young LLP and Chris K. Halterman, Executive Director, Advisory

April 2018 SOC for cybersecurity a backgrounder Acknowledgments Special thanks to Francette Bueno, Senior Manager, Advisory Services, Ernst & Young LLP and Chris K. Halterman, Executive Director, Advisory

A SERVICE ORGANIZATION S GUIDE SOC 1, 2, & 3 REPORTS

A SERVICE ORGANIZATION S GUIDE SOC 1, 2, & 3 REPORTS Introduction If you re a growing service organization, whether a technology provider, financial services corporation, healthcare company, or professional

A SERVICE ORGANIZATION S GUIDE SOC 1, 2, & 3 REPORTS Introduction If you re a growing service organization, whether a technology provider, financial services corporation, healthcare company, or professional

Safeguarding unclassified controlled technical information (UCTI)

") Safeguarding unclassified controlled technical information (UCTI) An overview Government Contract Services Bulletin Safeguarding UCTI An overview On November 18, 2013, the Department of Defense (DoD) issued

Safeguarding unclassified controlled technical information (UCTI) An overview Government Contract Services Bulletin Safeguarding UCTI An overview On November 18, 2013, the Department of Defense (DoD) issued

WHICH SOC REPORT IS RIGHT FOR YOUR CLIENT?

CPAs & ADVISORS STRATEGIC ALLIANCE WEBINAR SERIES WHICH SOC REPORT IS RIGHT FOR YOUR CLIENT? June 20, 2017 Cindy Boyle TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided

CPAs & ADVISORS STRATEGIC ALLIANCE WEBINAR SERIES WHICH SOC REPORT IS RIGHT FOR YOUR CLIENT? June 20, 2017 Cindy Boyle TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided

Audit Considerations Relating to an Entity Using a Service Organization

An Entity Using a Service Organization 355 AU-C Section 402 Audit Considerations Relating to an Entity Using a Service Organization Source: SAS No. 122; SAS No. 128; SAS No. 130. Effective for audits of

An Entity Using a Service Organization 355 AU-C Section 402 Audit Considerations Relating to an Entity Using a Service Organization Source: SAS No. 122; SAS No. 128; SAS No. 130. Effective for audits of

Protecting your data. EY s approach to data privacy and information security

Protecting your data EY s approach to data privacy and information security Digital networks are a key enabler in the globalization of business. They dramatically enhance our ability to communicate, share

Protecting your data EY s approach to data privacy and information security Digital networks are a key enabler in the globalization of business. They dramatically enhance our ability to communicate, share

SOC Reports The 2017 Update: What s new, What s not, and What you should be doing with the SOC Reports you receive! Presented by Jeff Pershing

SOC Reports The 2017 Update What s new, What s not, and What you should be doing with the SOC Reports you receive! presented to Northeast Ohio ISACA Thursday, April 20, 2017 Jeff Pershing, CISA, CISM,

SOC Reports The 2017 Update What s new, What s not, and What you should be doing with the SOC Reports you receive! presented to Northeast Ohio ISACA Thursday, April 20, 2017 Jeff Pershing, CISA, CISM,

IT Attestation in the Cloud Era

IT Attestation in the Cloud Era The need for increased assurance over outsourced operations/ controls April 2013 Symeon Kalamatianos M.Sc., CISA, CISM Senior Manager, IT Risk Consulting Contents Introduction

IT Attestation in the Cloud Era The need for increased assurance over outsourced operations/ controls April 2013 Symeon Kalamatianos M.Sc., CISA, CISM Senior Manager, IT Risk Consulting Contents Introduction

SSAE 18 & new SOC approach to compliance. Moderator Name: Patricio Garcia Managing Partner ControlCase Attestation Services

SSAE 18 & new SOC approach to compliance Moderator Name: Patricio Garcia Managing Partner ControlCase Attestation Services Agenda 1. SSAE 18 overview 2. SOC 2 + 3. 2017 Trust Services Criteria SSAE 18

SSAE 18 & new SOC approach to compliance Moderator Name: Patricio Garcia Managing Partner ControlCase Attestation Services Agenda 1. SSAE 18 overview 2. SOC 2 + 3. 2017 Trust Services Criteria SSAE 18

Introduction. When it comes to GDPR compliance, is OK for now enough? Minds made for protecting financial services

When it comes to GDPR compliance, is OK for now enough? EY CertifyPoint s GDPR certification process will help you achieve and demonstrate compliance. Minds made for protecting financial services Introduction

When it comes to GDPR compliance, is OK for now enough? EY CertifyPoint s GDPR certification process will help you achieve and demonstrate compliance. Minds made for protecting financial services Introduction

SERVICE ORGANIZATION CONTROL (SOC) REPORTS: WHAT ARE THEY?

REPORTS: WHAT ARE THEY?") WHITE PAPER SERVICE ORGANIZATION CONTROL (SOC) REPORTS: WHAT ARE THEY? JEFF COOK DIRECTOR CPA, CITP, CIPT, CISA North America Europe 877.224.8077 info@coalfire.com coalfire.com TABLE OF CONTENTS Summary...

WHITE PAPER SERVICE ORGANIZATION CONTROL (SOC) REPORTS: WHAT ARE THEY? JEFF COOK DIRECTOR CPA, CITP, CIPT, CISA North America Europe 877.224.8077 info@coalfire.com coalfire.com TABLE OF CONTENTS Summary...

Exploring Emerging Cyber Attest Requirements

Exploring Emerging Cyber Attest Requirements With a focus on SOC for Cybersecurity ( Cyber Attest ) Introductions and Overview Audrey Katcher Partner, RubinBrown LLP AICPA volunteer: AICPA SOC2 Guide Working

Exploring Emerging Cyber Attest Requirements With a focus on SOC for Cybersecurity ( Cyber Attest ) Introductions and Overview Audrey Katcher Partner, RubinBrown LLP AICPA volunteer: AICPA SOC2 Guide Working

SAS 70 Audit Concepts. and Benefits JAYACHANDRAN.B,CISA,CISM. August 2010

JAYACHANDRAN.B,CISA,CISM jb@esecurityaudit.com August 2010 SAS 70 Audit Concepts and Benefits Agenda Compliance requirements Overview Business Environment IT Governance and Compliance Management Vendor

JAYACHANDRAN.B,CISA,CISM jb@esecurityaudit.com August 2010 SAS 70 Audit Concepts and Benefits Agenda Compliance requirements Overview Business Environment IT Governance and Compliance Management Vendor

SOC Lessons Learned and Reporting Changes

SOC Lessons Learned and Reporting Changes Dec. 16, 2014 Your Presenters Today Arshad Ahmed, CISA, CISSP, CPA Leader of SOC and Technology Risk Services for Crowe Rod Smith, CISA, CPA Thought Leader for

SOC Lessons Learned and Reporting Changes Dec. 16, 2014 Your Presenters Today Arshad Ahmed, CISA, CISSP, CPA Leader of SOC and Technology Risk Services for Crowe Rod Smith, CISA, CPA Thought Leader for

Information for entity management. April 2018

Information for entity management April 2018 Note to readers: The purpose of this document is to assist management with understanding the cybersecurity risk management examination that can be performed

Information for entity management April 2018 Note to readers: The purpose of this document is to assist management with understanding the cybersecurity risk management examination that can be performed

Mastering SOC-1 Attestation Reports Under SSAE 16: Auditing Service Organizations Controls in the Cloud

FOR LIVE POGRAM ONLY Mastering SOC-1 Attestation Reports Under SSAE 16: Auditing Service Organizations Controls in the Cloud TUESDAY, AUGUST 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE POGRAM ONLY Mastering SOC-1 Attestation Reports Under SSAE 16: Auditing Service Organizations Controls in the Cloud TUESDAY, AUGUST 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Understanding and Evaluating Service Organization Controls (SOC) Reports

Reports") Understanding and Evaluating Service Organization Controls (SOC) Reports Kevin Sear, CPA, CIA, CISA, CFE, CGMA Agenda 1. Why are SOC reports important? 2. Understanding the new SOC-1, SOC-2, and SOC-3

Understanding and Evaluating Service Organization Controls (SOC) Reports Kevin Sear, CPA, CIA, CISA, CFE, CGMA Agenda 1. Why are SOC reports important? 2. Understanding the new SOC-1, SOC-2, and SOC-3

Step 1: Open browser to navigate to the data science challenge home page

Step 1: Open browser to navigate to the data science challenge home page https://datascience.ey.com/ Step 2: Logging in You will need to create an account if you are a new user. Click the sign up button

Step 1: Open browser to navigate to the data science challenge home page https://datascience.ey.com/ Step 2: Logging in You will need to create an account if you are a new user. Click the sign up button

COBIT 5 With COSO 2013

Integrating COBIT 5 With COSO 2013 Stephen Head Senior Manager, IT Risk Advisory Services 1 Our Time This Evening Importance of Governance COBIT 5 Overview COSO Overview Mapping These Frameworks Stakeholder

Integrating COBIT 5 With COSO 2013 Stephen Head Senior Manager, IT Risk Advisory Services 1 Our Time This Evening Importance of Governance COBIT 5 Overview COSO Overview Mapping These Frameworks Stakeholder

Big data privacy in Australia

Five-article series Big data privacy in Australia Three actions you can take towards compliance Article 5 Big data and privacy Three actions you can take towards compliance There are three actions that

Five-article series Big data privacy in Australia Three actions you can take towards compliance Article 5 Big data and privacy Three actions you can take towards compliance There are three actions that

CSF to Support SOC 2 Repor(ng

CSF to Support SOC 2 Repor(ng Ken Vander Wal, CPA, CISA, HCISPP Chief Compliance Officer, HITRUST * ken.vanderwal@hitrustalliance.net Agenda Introduction to SOC Reporting SOC 2 and HITRUST CSF AICPA and

CSF to Support SOC 2 Repor(ng Ken Vander Wal, CPA, CISA, HCISPP Chief Compliance Officer, HITRUST * ken.vanderwal@hitrustalliance.net Agenda Introduction to SOC Reporting SOC 2 and HITRUST CSF AICPA and

Achieving third-party reporting proficiency with SOC 2+

Achieving third-party reporting proficiency with SOC 2+ Achieving third-party reporting proficiency with SOC 2+ Today s organizations do business within a broad ecosystem. Customers, partners, agents,

Achieving third-party reporting proficiency with SOC 2+ Achieving third-party reporting proficiency with SOC 2+ Today s organizations do business within a broad ecosystem. Customers, partners, agents,

California ISO Audit Results for 2011 SSAE 16 & Looking Forward for 2012 December 15, 2011

www.pwc.com California ISO Audit Results for 2011 SSAE 16 & Looking Forward for 2012 December 15, 2011 Agenda SSAE 16 Background Results of Audit Scope of Audit Looking Forward Closing Thoughts Slide 1

www.pwc.com California ISO Audit Results for 2011 SSAE 16 & Looking Forward for 2012 December 15, 2011 Agenda SSAE 16 Background Results of Audit Scope of Audit Looking Forward Closing Thoughts Slide 1

SOC 3 for Security and Availability

SOC 3 for Security and Availability Independent Practioner s Trust Services Report For the Period October 1, 2015 through September 30, 2016 Independent SOC 3 Report for the Security and Availability Trust

SOC 3 for Security and Availability Independent Practioner s Trust Services Report For the Period October 1, 2015 through September 30, 2016 Independent SOC 3 Report for the Security and Availability Trust

Citation for published version (APA): Berthing, H. H. (2014). Vision for IT Audit Abstract from Nordic ISACA Conference 2014, Oslo, Norway.

: Berthing, H. H. (2014). Vision for IT Audit Abstract from Nordic ISACA Conference 2014, Oslo, Norway.") Aalborg Universitet Vision for IT Audit 2020 Berthing, Hans Henrik Aabenhus Publication date: 2014 Document Version Early version, also known as pre-print Link to publication from Aalborg University Citation

Aalborg Universitet Vision for IT Audit 2020 Berthing, Hans Henrik Aabenhus Publication date: 2014 Document Version Early version, also known as pre-print Link to publication from Aalborg University Citation

HITRUST CSF: One Framework

HITRUST CSF: One Framework Leveraging the HITRUST CSF to Support ISO, HIPAA, & NIST Implementation and Compliance, and SSAE 16 SOC Reporting Dr. Bryan Cline, CISSP-ISSEP, CISM, CISA, CCSFP, HCISPP Senior

HITRUST CSF: One Framework Leveraging the HITRUST CSF to Support ISO, HIPAA, & NIST Implementation and Compliance, and SSAE 16 SOC Reporting Dr. Bryan Cline, CISSP-ISSEP, CISM, CISA, CCSFP, HCISPP Senior

IGNITING GROWTH. Why a SOC Report Makes All the Difference

IGNITING GROWTH Why a SOC Report Makes All the Difference Many service organizations depend on the integrity of their control environment to protect their business as well as that of their customers. With

IGNITING GROWTH Why a SOC Report Makes All the Difference Many service organizations depend on the integrity of their control environment to protect their business as well as that of their customers. With

The SOC 2 Compliance Handbook:

The SOC 2 Compliance Handbook: Your guide to SOC 2 Audit Success The SOC 2 Compliance Handbook Page 2 Table of Contents Abstract 3 Why am I being asked about SOC Compliance? 4 What s the difference between

The SOC 2 Compliance Handbook: Your guide to SOC 2 Audit Success The SOC 2 Compliance Handbook Page 2 Table of Contents Abstract 3 Why am I being asked about SOC Compliance? 4 What s the difference between

SAS 70 revised. ISAE 3402 will focus on financial reporting control procedures. Compact_ IT Advisory 41. Introduction

Compact_ IT Advisory 41 SAS 70 revised ISAE 3402 will focus on financial reporting control procedures Jaap van Beek and Marco Francken J.J. van Beek is a partner at KPMG IT Advisory. He has over twenty-years

Compact_ IT Advisory 41 SAS 70 revised ISAE 3402 will focus on financial reporting control procedures Jaap van Beek and Marco Francken J.J. van Beek is a partner at KPMG IT Advisory. He has over twenty-years

Canada Highlights. Cybersecurity: Do you know which protective measures will make your company cyber resilient?

Canada Highlights Cybersecurity: Do you know which protective measures will make your company cyber resilient? 21 st Global Information Security Survey 2018 2019 1 Canada highlights According to the EY

Canada Highlights Cybersecurity: Do you know which protective measures will make your company cyber resilient? 21 st Global Information Security Survey 2018 2019 1 Canada highlights According to the EY

SOC Updates: Understanding SOC for Cybersecurity and SSAE 18. May 23, 2017

SOC Updates: Understanding SOC for Cybersecurity and SSAE 18 May 23, 2017 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

SOC Updates: Understanding SOC for Cybersecurity and SSAE 18 May 23, 2017 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

What s new in EY Atlas. November 2018

November 2018 EY tlas is regularly evolving and being enhanced to make your experience with the tool even better. This document highlights the new features and enhancements made since EY tlas was launched

November 2018 EY tlas is regularly evolving and being enhanced to make your experience with the tool even better. This document highlights the new features and enhancements made since EY tlas was launched

Auditing IT General Controls

Auditing IT General Controls Amanthi Pendegraft and Nadine Yassine September 27, 2017 Agenda Introduction and Objectives IT Audit Fundamentals IT General Controls Overview Access to Programs and Data Program

Auditing IT General Controls Amanthi Pendegraft and Nadine Yassine September 27, 2017 Agenda Introduction and Objectives IT Audit Fundamentals IT General Controls Overview Access to Programs and Data Program

International Auditing and Assurance Standards Board (IAASB) International Federation of Accountants 545 Fifth Avenue, 14 th Floor New York, NY 10017

International Federation of Accountants 545 Fifth Avenue, 14 th Floor New York, NY 10017") 3701 Algonquin Road, Suite 1010 Telephone: 847.253.1545 Rolling Meadows, Illinois 60008, USA Facsimile: 847.253.1443 Web Sites: www.isaca.org and www.itgi.org 25 April 2008 International Auditing and Assurance

3701 Algonquin Road, Suite 1010 Telephone: 847.253.1545 Rolling Meadows, Illinois 60008, USA Facsimile: 847.253.1443 Web Sites: www.isaca.org and www.itgi.org 25 April 2008 International Auditing and Assurance

EY s Data Privacy Services. January 2019

EY s Data Privacy Services January 2019 Introduction Data privacy encompasses the rights and obligations of individuals and organizations with respect to the collection, use, disclosure, and retention

EY s Data Privacy Services January 2019 Introduction Data privacy encompasses the rights and obligations of individuals and organizations with respect to the collection, use, disclosure, and retention

Forensic analysis with leading technology: the intelligent connection Fraud Investigation & Dispute Services

Forensic Technology & Discovery Services Forensic analysis with leading technology: the intelligent connection Fraud Investigation & Dispute Services Forensic Technology & Discovery Services EY s Forensic

Forensic Technology & Discovery Services Forensic analysis with leading technology: the intelligent connection Fraud Investigation & Dispute Services Forensic Technology & Discovery Services EY s Forensic

INTO THE CLOUD WHAT YOU NEED TO KNOW ABOUT ADOPTION AND ENSURING COMPLIANCE

INTO THE CLOUD WHAT YOU NEED TO KNOW ABOUT ADOPTION AND ENSURING COMPLIANCE INTRODUCTION AGENDA 01. Overview of Cloud Services 02. Cloud Computing Compliance Framework 03. Cloud Adoption and Enhancing

INTO THE CLOUD WHAT YOU NEED TO KNOW ABOUT ADOPTION AND ENSURING COMPLIANCE INTRODUCTION AGENDA 01. Overview of Cloud Services 02. Cloud Computing Compliance Framework 03. Cloud Adoption and Enhancing

Tax News Update: Global Edition (GTNU) User Guide

User Guide") Tax News Update: Global Edition (GTNU) User Guide Agenda GTNU introduction Highlights How to access GTNU How to set up email preferences Browsing for content Refinement panel Searching for content Page

Tax News Update: Global Edition (GTNU) User Guide Agenda GTNU introduction Highlights How to access GTNU How to set up email preferences Browsing for content Refinement panel Searching for content Page

SAS70 Type II Reports Use and Interpretation for SOX

SAS70 Type II Reports Use and Interpretation for SOX November 19, 2007 Presented by: Erin Erickson, Senior Manager Enterprise Governance and Brenda Karl, Director Technology Risk Management Agenda Background

SAS70 Type II Reports Use and Interpretation for SOX November 19, 2007 Presented by: Erin Erickson, Senior Manager Enterprise Governance and Brenda Karl, Director Technology Risk Management Agenda Background

Workday s Robust Privacy Program

Workday s Robust Privacy Program Workday s Robust Privacy Program Introduction Workday is a leading provider of enterprise cloud applications for human resources and finance. Founded in 2005 by Dave Duffield

Workday s Robust Privacy Program Workday s Robust Privacy Program Introduction Workday is a leading provider of enterprise cloud applications for human resources and finance. Founded in 2005 by Dave Duffield

Studio Guggino and Newtonpartner S.r.l. a team of professionals at the service of your Company

Studio Guggino and Newtonpartner S.r.l. a team of professionals at the service of your Company To get where the others fail, we have to achieve even higher goals www.sas70.it MISSION Our Mission consists

Studio Guggino and Newtonpartner S.r.l. a team of professionals at the service of your Company To get where the others fail, we have to achieve even higher goals www.sas70.it MISSION Our Mission consists

Article II - Standards Section V - Continuing Education Requirements

Article II - Standards Section V - Continuing Education Requirements 2.5.1 CONTINUING PROFESSIONAL EDUCATION Internal auditors are responsible for maintaining their knowledge and skills. They should update

Article II - Standards Section V - Continuing Education Requirements 2.5.1 CONTINUING PROFESSIONAL EDUCATION Internal auditors are responsible for maintaining their knowledge and skills. They should update

2018 HIPAA One All Rights Reserved. Beyond HIPAA Compliance to Certification

2018 HIPAA One All Rights Reserved. Beyond HIPAA Compliance to Certification Presenters Jared Hamilton CISSP CCSK, CCSFP, MCSE:S Healthcare Cybersecurity Leader, Crowe Horwath Erika Del Giudice CISA, CRISC,

2018 HIPAA One All Rights Reserved. Beyond HIPAA Compliance to Certification Presenters Jared Hamilton CISSP CCSK, CCSFP, MCSE:S Healthcare Cybersecurity Leader, Crowe Horwath Erika Del Giudice CISA, CRISC,

ADVANCED AUDIT AND ASSURANCE

ADVANCED AUDIT AND ASSURANCE CPA PROGRAM SUBJECT OUTLINE The Advanced Audit and Assurance subject provides a body of knowledge for you to understand the nature and diversity of audit and assurance engagements.

ADVANCED AUDIT AND ASSURANCE CPA PROGRAM SUBJECT OUTLINE The Advanced Audit and Assurance subject provides a body of knowledge for you to understand the nature and diversity of audit and assurance engagements.

Hong Kong Institute of Certified Public Accountants Practising Certificate ("PC") Business Assurance

Business Assurance") Hong Kong Institute of Certified Public Accountants Practising Certificate ("PC") Business Assurance Examinable Auditing Standards December 2017 Session and June 2018 session This document contains the

Hong Kong Institute of Certified Public Accountants Practising Certificate ("PC") Business Assurance Examinable Auditing Standards December 2017 Session and June 2018 session This document contains the

Within our recommendations for editorial changes, additions are noted in bold underline and deletions in strike-through.

1633 Broadway New York, NY 10019-6754 Mr. Jim Sylph Executive Director, Professional Standards International Federation of Accountants 545 Fifth Avenue, 14th Floor New York, NY 10017 Dear Mr. Sylph: We

1633 Broadway New York, NY 10019-6754 Mr. Jim Sylph Executive Director, Professional Standards International Federation of Accountants 545 Fifth Avenue, 14th Floor New York, NY 10017 Dear Mr. Sylph: We

Google Cloud & the General Data Protection Regulation (GDPR)

") Google Cloud & the General Data Protection Regulation (GDPR) INTRODUCTION General Data Protection Regulation (GDPR) On 25 May 2018, the most significant piece of European data protection legislation to

Google Cloud & the General Data Protection Regulation (GDPR) INTRODUCTION General Data Protection Regulation (GDPR) On 25 May 2018, the most significant piece of European data protection legislation to

26 February Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, NW Washington, DC

3701 Algonquin Road, Suite 1010 Telephone: 847.253.1545 Rolling Meadows, Illinois 60008, USA Facsimile: 847.253.1443 Web Sites: www.isaca.org and www.itgi.org 26 February 2007 Office of the Secretary Public

3701 Algonquin Road, Suite 1010 Telephone: 847.253.1545 Rolling Meadows, Illinois 60008, USA Facsimile: 847.253.1443 Web Sites: www.isaca.org and www.itgi.org 26 February 2007 Office of the Secretary Public

Does a SAS 70 Audit Leave you at Risk of a Security Exposure or Failure to Comply with FISMA?

Does a SAS 70 Audit Leave you at Risk of a Security Exposure or Failure to Comply with FISMA? A brief overview of security requirements for Federal government agencies applicable to contracted IT services,

Does a SAS 70 Audit Leave you at Risk of a Security Exposure or Failure to Comply with FISMA? A brief overview of security requirements for Federal government agencies applicable to contracted IT services,

Robert Brammer. Senior Advisor to the Internet2 CEO Internet2 NET+ Security Assessment Forum. 8 April 2014

Robert Brammer Senior Advisor to the Internet2 CEO rfbtech@internet2.edu Internet2 NET+ Security Assessment Forum 8 April 2014 INTERNET2 NET+ Security Initiative Primary objective -- develop guidance to

Robert Brammer Senior Advisor to the Internet2 CEO rfbtech@internet2.edu Internet2 NET+ Security Assessment Forum 8 April 2014 INTERNET2 NET+ Security Initiative Primary objective -- develop guidance to

Quality Management Systems (ISO 9001:2015 and ISO 29001) Lead Auditor training (EY/IMSA Q03)

Lead Auditor training (EY/IMSA Q03)") Quality Management Systems (ISO 9001:2015 and ISO 29001) Lead Auditor training (EY/IMSA Q03) Doha, 4 8 March 2018 IMSA is an IRCA/CQI Approved Training Provider Contents Section 1: About the program 04

Quality Management Systems (ISO 9001:2015 and ISO 29001) Lead Auditor training (EY/IMSA Q03) Doha, 4 8 March 2018 IMSA is an IRCA/CQI Approved Training Provider Contents Section 1: About the program 04

HIPAA Privacy, Security and Breach Notification

HIPAA Privacy, Security and Breach Notification HCCA East Central Regional Annual Conference October 2013 Disclaimer The information contained in this document is provided by KPMG LLP for general guidance

HIPAA Privacy, Security and Breach Notification HCCA East Central Regional Annual Conference October 2013 Disclaimer The information contained in this document is provided by KPMG LLP for general guidance

Cyber Security in M&A. Joshua Stone, CIA, CFE, CISA

Cyber Security in M&A Joshua Stone, CIA, CFE, CISA Agenda About Whitley Penn, LLP The Threat Landscape Changed Cybersecurity Due Diligence Privacy Practices Cybersecurity Practices Costs of a Data Breach

Cyber Security in M&A Joshua Stone, CIA, CFE, CISA Agenda About Whitley Penn, LLP The Threat Landscape Changed Cybersecurity Due Diligence Privacy Practices Cybersecurity Practices Costs of a Data Breach

EY Training. Project Management Professional PMP. Exam preparatory course. 30 September 4 October 2018

EY Training Project Management Professional PMP Exam preparatory course 30 September 4 October 2018 Contents Introduction 04 Membership and examination 05 Key information 06 Registration form 07 Introduction

EY Training Project Management Professional PMP Exam preparatory course 30 September 4 October 2018 Contents Introduction 04 Membership and examination 05 Key information 06 Registration form 07 Introduction

Credit Union Service Organization Compliance

Credit Union Service Organization Compliance How do SOC reporting and PCI requirements affect your overall compliance strategy? May 15 2012 Your Speakers Dennis Lavin Credit Union Assurance Partner Moderator

Credit Union Service Organization Compliance How do SOC reporting and PCI requirements affect your overall compliance strategy? May 15 2012 Your Speakers Dennis Lavin Credit Union Assurance Partner Moderator

The value of visibility. Cybersecurity risk management examination

The value of visibility Cybersecurity risk management examination Welcome to the "new normal" Cyberattacks are inevitable. In fact, it s no longer a question of if a breach will occur but when. Cybercriminals

The value of visibility Cybersecurity risk management examination Welcome to the "new normal" Cyberattacks are inevitable. In fact, it s no longer a question of if a breach will occur but when. Cybercriminals

BENEFITS of MEMBERSHIP FOR YOUR INSTITUTION

PROFILE The Fiduciary and Investment Risk Management Association, Inc. (FIRMA ) is the leading provider of fiduciary and investment risk management education and networking to the fiduciary and investment

PROFILE The Fiduciary and Investment Risk Management Association, Inc. (FIRMA ) is the leading provider of fiduciary and investment risk management education and networking to the fiduciary and investment

REPORT 2015/149 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/149 Audit of the information and communications technology operations in the Investment Management Division of the United Nations Joint Staff Pension Fund Overall results

INTERNAL AUDIT DIVISION REPORT 2015/149 Audit of the information and communications technology operations in the Investment Management Division of the United Nations Joint Staff Pension Fund Overall results

Performing a Vendor Security Review TCTC 2017 FALL EVENT PRESENTER: KATIE MCINTOSH

Performing a Vendor Security Review TCTC 2017 FALL EVENT PRESENTER: KATIE MCINTOSH 1 Speaker Bio Katie McIntosh, CISM, CRISC, CISA, CIA, CRMA, is the Cyber Security Specialist for Central Hudson Gas &

Performing a Vendor Security Review TCTC 2017 FALL EVENT PRESENTER: KATIE MCINTOSH 1 Speaker Bio Katie McIntosh, CISM, CRISC, CISA, CIA, CRMA, is the Cyber Security Specialist for Central Hudson Gas &

Cyber Risks in the Boardroom Conference

Cyber Risks in the Boardroom Conference Managing Business, Legal and Reputational Risks Perspectives for Directors and Executive Officers Preparing Your Company to Identify, Mitigate and Respond to Risks

Cyber Risks in the Boardroom Conference Managing Business, Legal and Reputational Risks Perspectives for Directors and Executive Officers Preparing Your Company to Identify, Mitigate and Respond to Risks

Cybersecurity requirements for financial services companies

Cybersecurity requirements for financial services companies Overview of the finalized Cybersecurity Requirements from the New York State Department of Financial Services (DFS) February 2017 Overview This

Cybersecurity requirements for financial services companies Overview of the finalized Cybersecurity Requirements from the New York State Department of Financial Services (DFS) February 2017 Overview This

ISAE 3402 and SSAE 16 (replacing SAS 70) Reinforcing confidence through demonstration of effective controls

Reinforcing confidence through demonstration of effective controls") ISAE 3402 and SSAE 16 (replacing SAS 70) Reinforcing confidence through demonstration of effective controls ISAE 3402 and SSAE 16 defined Overview of service organisation control reports Service organisation

ISAE 3402 and SSAE 16 (replacing SAS 70) Reinforcing confidence through demonstration of effective controls ISAE 3402 and SSAE 16 defined Overview of service organisation control reports Service organisation

Project Management Professional PMP. Exam preparatory course

Project Management Professional PMP Exam preparatory course Contents Introduction 03 Agenda 05 Key information 06 Introduction What is the PMP? The Project Management Professional (PMP ) is one of the

Project Management Professional PMP Exam preparatory course Contents Introduction 03 Agenda 05 Key information 06 Introduction What is the PMP? The Project Management Professional (PMP ) is one of the

Testers vs Writers: Pen tests Quality in Assurance Projects. 10 November Defcamp7

Testers vs Writers: Pen tests Quality in Assurance Projects 10 November 2016 @ Defcamp7 Contents INTRODUCTION CONTEXT WHAT ABOUT AUDITING STANDARDS WHAT ABOUT INDEPENDENCE PEN TEST BETWEEN REGULATORY AND

Testers vs Writers: Pen tests Quality in Assurance Projects 10 November 2016 @ Defcamp7 Contents INTRODUCTION CONTEXT WHAT ABOUT AUDITING STANDARDS WHAT ABOUT INDEPENDENCE PEN TEST BETWEEN REGULATORY AND

WHITE PAPER. Title. Managed Services for SAS Technology

WHITE PAPER Hosted Title Managed Services for SAS Technology ii Contents Performance... 1 Optimal storage and sizing...1 Secure, no-hassle access...2 Dedicated computing infrastructure...2 Early and pre-emptive

WHITE PAPER Hosted Title Managed Services for SAS Technology ii Contents Performance... 1 Optimal storage and sizing...1 Secure, no-hassle access...2 Dedicated computing infrastructure...2 Early and pre-emptive

Weighing in on the Benefits of a SAS 70 Audit for Third Party Administrators

Weighing in on the Benefits of a SAS 70 Audit for Third Party Administrators With increasing oversight and growing demands for industry regulations, third party assurance has never been under a keener

Weighing in on the Benefits of a SAS 70 Audit for Third Party Administrators With increasing oversight and growing demands for industry regulations, third party assurance has never been under a keener

The HIPAA Security & Privacy Rule How Municipalities Can Prepare for Compliance

The HIPAA Security & Privacy Rule How Municipalities Can Prepare for Compliance Russell L. Jones Partner Health Sciences Sector Deloitte & Touche LLP Security & Privacy IMLA 2013 Annual Conference San

The HIPAA Security & Privacy Rule How Municipalities Can Prepare for Compliance Russell L. Jones Partner Health Sciences Sector Deloitte & Touche LLP Security & Privacy IMLA 2013 Annual Conference San

Internal Audit Report. Electronic Bidding and Contract Letting TxDOT Office of Internal Audit

Internal Audit Report Electronic Bidding and Contract Letting TxDOT Office of Internal Audit Objective Review of process controls and service delivery of the TxDOT electronic bidding process. Opinion Based

Internal Audit Report Electronic Bidding and Contract Letting TxDOT Office of Internal Audit Objective Review of process controls and service delivery of the TxDOT electronic bidding process. Opinion Based

Information Technology Security Plan Policies, Controls, and Procedures Identify Governance ID.GV

Information Technology Security Plan Policies, Controls, and Procedures Identify Governance ID.GV Location: https://www.pdsimplified.com/ndcbf_pdframework/nist_csf_prc/documents/identify/ndcbf _ITSecPlan_IDGV2017.pdf

Information Technology Security Plan Policies, Controls, and Procedures Identify Governance ID.GV Location: https://www.pdsimplified.com/ndcbf_pdframework/nist_csf_prc/documents/identify/ndcbf _ITSecPlan_IDGV2017.pdf

FedRAMP: Understanding Agency and Cloud Provider Responsibilities

May 2013 Walter E. Washington Convention Center Washington, DC FedRAMP: Understanding Agency and Cloud Provider Responsibilities Matthew Goodrich, JD FedRAMP Program Manager US General Services Administration

May 2013 Walter E. Washington Convention Center Washington, DC FedRAMP: Understanding Agency and Cloud Provider Responsibilities Matthew Goodrich, JD FedRAMP Program Manager US General Services Administration

CIP Cyber Security Configuration Change Management and Vulnerability Assessments

Standard Development Timeline This section is maintained by the drafting team during the development of the standard and will be removed when the standard becomes effective. Development Steps Completed

Standard Development Timeline This section is maintained by the drafting team during the development of the standard and will be removed when the standard becomes effective. Development Steps Completed

IT Audit Process. Prof. Mike Romeu. January 30, IT Audit Process. Prof. Mike Romeu

January 30, 2017 1 Corporate Structures Shareholders Governance Level: Board of Directors External Director CFO CEO Legal Counsel External Director Responsible for: Evaluate Direct Monitor Internal Directors

January 30, 2017 1 Corporate Structures Shareholders Governance Level: Board of Directors External Director CFO CEO Legal Counsel External Director Responsible for: Evaluate Direct Monitor Internal Directors

Business Assurance for the 21st Century

14/07/2011 Navigating the Information Assurance landscape AUTHORS Niall Browne NAME AFFILIATION Shared Assessments Program Michael de Crespigny (CEO) Jim Reavis Kurt Roemer Raj Samani Information Security

14/07/2011 Navigating the Information Assurance landscape AUTHORS Niall Browne NAME AFFILIATION Shared Assessments Program Michael de Crespigny (CEO) Jim Reavis Kurt Roemer Raj Samani Information Security

Embedded SIM Study. September 2015 update

Embedded SIM Study September 2015 update Executive summary Following a first white paper drawing upon interviews with mobile network operators in 3Q 2014, EY decided to perform a second round of interviews

Embedded SIM Study September 2015 update Executive summary Following a first white paper drawing upon interviews with mobile network operators in 3Q 2014, EY decided to perform a second round of interviews

Cyber Security Reliability Standards CIP V5 Transition Guidance:

Cyber Security Reliability Standards CIP V5 Transition Guidance: ERO Compliance and Enforcement Activities during the Transition to the CIP Version 5 Reliability Standards To: Regional Entities and Responsible

Cyber Security Reliability Standards CIP V5 Transition Guidance: ERO Compliance and Enforcement Activities during the Transition to the CIP Version 5 Reliability Standards To: Regional Entities and Responsible

The HITRUST CSF. A Revolutionary Way to Protect Electronic Health Information

The HITRUST CSF A Revolutionary Way to Protect Electronic Health Information June 2015 The HITRUST CSF 2 Organizations in the healthcare industry are under immense pressure to improve quality, reduce complexity,

The HITRUST CSF A Revolutionary Way to Protect Electronic Health Information June 2015 The HITRUST CSF 2 Organizations in the healthcare industry are under immense pressure to improve quality, reduce complexity,

Error! No text of specified style in document.

Error! No text of specified style in document. Error! Use the Home tab to apply Section title to the text that you want to appear here. CFD Independent Auditor Report on CFD Allocation Round 2 4 September

Error! No text of specified style in document. Error! Use the Home tab to apply Section title to the text that you want to appear here. CFD Independent Auditor Report on CFD Allocation Round 2 4 September

Article I - Administrative Bylaws Section IV - Coordinator Assignments

3 Article I - Administrative Bylaws Section IV - Coordinator Assignments 1.4.1 ASSIGNMENT OF COORDINATORS To fulfill the duties of the Fiscal Control and Internal Auditing Act (30 ILCS 10/2005), the Board

3 Article I - Administrative Bylaws Section IV - Coordinator Assignments 1.4.1 ASSIGNMENT OF COORDINATORS To fulfill the duties of the Fiscal Control and Internal Auditing Act (30 ILCS 10/2005), the Board

How to avoid storms in the cloud. The Australian experience and global trends

How to avoid storms in the cloud The Australian experience and global trends Discussion Topics 1. Understanding Cloud and Benefits 2. KPMG research The Australian Experience and Global Trends 3. Considerations

How to avoid storms in the cloud The Australian experience and global trends Discussion Topics 1. Understanding Cloud and Benefits 2. KPMG research The Australian Experience and Global Trends 3. Considerations

Introduction to AWS GoldBase

Introduction to AWS GoldBase A Solution to Automate Security, Compliance, and Governance in AWS October 2015 2015, Amazon Web Services, Inc. or its affiliates. All rights reserved. Notices This document

Introduction to AWS GoldBase A Solution to Automate Security, Compliance, and Governance in AWS October 2015 2015, Amazon Web Services, Inc. or its affiliates. All rights reserved. Notices This document

Global Specification Protocol for Organisations Certifying to an ISO Standard related to Market, Opinion and Social Research.

CONTENTS i. INTRODUCTION 3 ii. OVERVIEW SPECIFICATION PROTOCOL DOCUMENT DEVELOPMENT PROCESS 4 1. SCOPE 5 2. DEFINITIONS 5 3. REFERENCES 6 4. MANAGEMENT STANDARDS FOR APPROVED CERTIFICATION BODIES 6 4.1

CONTENTS i. INTRODUCTION 3 ii. OVERVIEW SPECIFICATION PROTOCOL DOCUMENT DEVELOPMENT PROCESS 4 1. SCOPE 5 2. DEFINITIONS 5 3. REFERENCES 6 4. MANAGEMENT STANDARDS FOR APPROVED CERTIFICATION BODIES 6 4.1

UNCONTROLLED IF PRINTED

161Thorn Hill Road Warrendale, PA 15086-7527 1. Scope 2. Definitions PROGRAM DOCUMENT PD 1000 Issue Date: 19-Apr-2015 Revision Date: 26-May-2015 INDUSTRY MANAGED ACCREDITATION PROGRAM DOCUMENT Table of

161Thorn Hill Road Warrendale, PA 15086-7527 1. Scope 2. Definitions PROGRAM DOCUMENT PD 1000 Issue Date: 19-Apr-2015 Revision Date: 26-May-2015 INDUSTRY MANAGED ACCREDITATION PROGRAM DOCUMENT Table of

HITRUST CSF Roadmap for 2018 and Beyond HITRUST Alliance.

HITRUST CSF Roadmap for 2018 and Beyond HITRUST CSF Roadmap 2017 HITRUST CSF v9 Update 21 CFR Part 11 (FDA electronic signatures) Add FFIEC IT Examination (InfoSec), FedRAMP, DHS Critical Resilience Review

HITRUST CSF Roadmap for 2018 and Beyond HITRUST CSF Roadmap 2017 HITRUST CSF v9 Update 21 CFR Part 11 (FDA electronic signatures) Add FFIEC IT Examination (InfoSec), FedRAMP, DHS Critical Resilience Review

EY Norwegian Cloud Maturity Survey Current and planned adoption of cloud services

EY Norwegian Cloud Maturity Survey 2019 Current and planned adoption of cloud services Contents 01 Cloud maturity 4 02 Drivers and challenges 6 03 Current usage 10 04 Future plans 16 05 About the survey

EY Norwegian Cloud Maturity Survey 2019 Current and planned adoption of cloud services Contents 01 Cloud maturity 4 02 Drivers and challenges 6 03 Current usage 10 04 Future plans 16 05 About the survey

IS Audit and Assurance Guideline 2002 Organisational Independence

IS Audit and Assurance Guideline 2002 Organisational Independence The specialised nature of information systems (IS) audit and assurance and the skills necessary to perform such engagements require standards

IS Audit and Assurance Guideline 2002 Organisational Independence The specialised nature of information systems (IS) audit and assurance and the skills necessary to perform such engagements require standards

REPORT 2015/186 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/186 Audit of information and communications technology operations in the Secretariat of the United Nations Joint Staff Pension Fund Overall results relating to the effective

INTERNAL AUDIT DIVISION REPORT 2015/186 Audit of information and communications technology operations in the Secretariat of the United Nations Joint Staff Pension Fund Overall results relating to the effective