United States Personal Device History and Forecast, April 2019

|

|

|

- Jean Thomas

- 5 years ago

- Views:

Transcription

1 United States Personal Device History and Forecast, April 2019 Table of Content Market Overview Forecasting Approach and Process Market Tables Next Five Years Major Causal Influences and Trends The United States Economy Unit Shipments Installed Base Penetration Density Replacement Rates Replacement Cycle Length Age of Retired/Removed Units Purpose and Location Hybrid PCs, 2-in-1 Product Forecast Tables Sources of Historical Data Methodology Total Available Market About Daniel Research Group

2 List of Tables United States Total Personal Devices Unit Shipments (K) United States Consumer Personal Devices Unit Shipments (K) United States Enterprise Personal Devices Unit Shipments (K) Desktop PCs -Fixed Creation United States Consumer Desktop PCs United States Enterprise Desktop PCs United States Consumer & Enterprise Desktop PCs Mobile PCs Mobile Creation and Capture United States Consumer Convertible Mobile PCs United States Consumer Traditional Mobile PCs United States Consumer Mobile PCs United States Enterprise Convertible Mobile PCs United States Enterprise Traditional Mobile PCs United States Enterprise Mobile PCs United States Consumer & Enterprise Convertible Mobile PCs United States Consumer & Enterprise Traditional Mobile PCs United States Consumer & Enterprise Mobile PCs Total PCs United States Consumer Total PCs United States Enterprise Total PCs United States Consumer & Enterprise Total PCs Tablets Mobile Creation and Capture, Delivery United States Consumer Slate Tablets United States Consumer Detachable Tablets United States Consumer Tablets United States Enterprise Slate Tablets United States Enterprise Detachable Tablets United States Enterprise Tablets United States Consumer & Enterprise Detachable Tablets United States Consumer & Enterprise Slate Tablets United States Consumer & Enterprise Tablets Mobile PCs and Tablets United States Consumer Mobile PCs & Tablets United States Enterprise Mobile PCs & Tablets United States Consumer & Enterprise Mobile PCs & Tablets

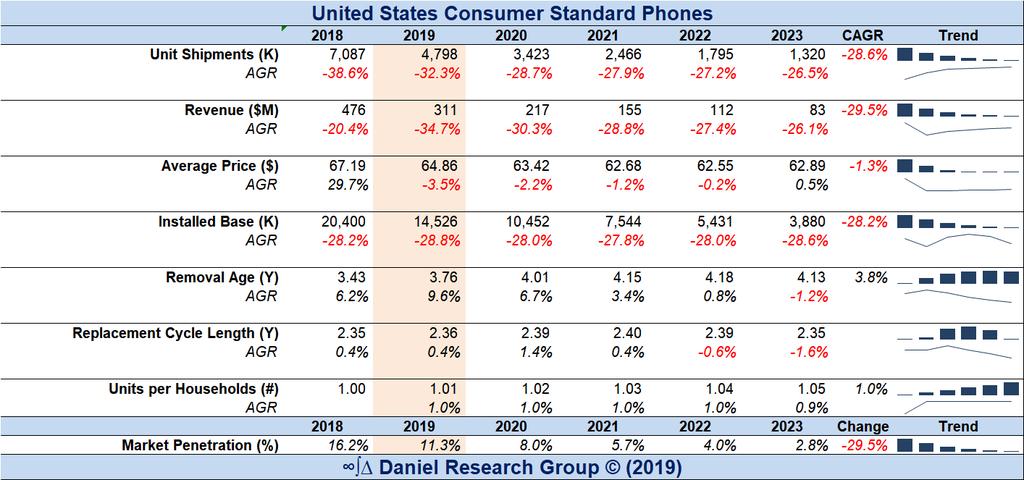

3 Total PCs and Tablets United States Consumer PCs & Tablets United States Enterprise PCs & Tablets United States Consumer & Enterprise PCs & Tablets Hybrid PC, 2-in-1 United States Consumer 2-in-1 Mobile PC & Tablets United States Enterprise 2-in-1 Mobile PC & Tablets United States Consumer & Enterprise 2-in-1 Mobile PC & Tablets Mobile Creation & Capture United States Consumer Detachable Mobile PCs & Tablets United States Enterprise Detachable Mobile PCs & Tablets United States Consumer & Enterprise Detachable Mobile PCs & Tablets Mobile Delivery United States Consumer e-readers United States Consumer Slate Tablets & e-readers United States Consumer & Enterprise Slate Tablets & e-readers Mobile Phones Mobile Communication United States Consumer Standard Phones United States Enterprise Standard Phones United States Consumer & Enterprise Standard Phones United States Consumer Smartphones United States Enterprise Smartphones United States Consumer & Enterprise Smartphones United States Consumer Mobile Phones United States Enterprise Mobile Phones United States Consumer & Enterprise Mobile Phones Total Personal Devices United States Consumer Personal Devices United States Enterprise Personal Devices United States Consumer & Enterprise Personal Devices

4 List of Chart Economy Congressional Budget Office Economic Forecasts, January 2019 Annual Growth Rate: Private, All Industries, All Size Classes Change in Percent of Employees by Size of Business, Change in Number of Business by Size Class, Unit Shipments United States Total Personal Computing Devices, Unit Shipments (K) United States Consumer Personal Computing Devices, Unit Shipments (K) United States Enterprise Personal Computing Devices, Unit Shipments (K) United States Personal Communications Device Market: Unit Shipments (K), United States Personal Devices 2019 Unit Shipments Annual Growth Rate United States Personal Devices Unit Shipments CAGR United States Personal Computing Devices, Percent of Unit Shipments, 2019 and 2023 Installed Base United States Total Personal Computing Devices, Installed Base (K) United States Consumer Personal Computing Devices, Installed Base (K) United States Enterprise Personal Computing Devices, Installed Base (K) United States Personal Communications Device Market: Installed Base (K), United States Personal Devices 2019 Installed Base Annual Growth Rate United States Personal Devices Installed Base CAGR United States Personal Computing Devices, Percent of Installed Base, 2019 and 2023 Penetration United States Personal Computing Device Market Penetration, , April 2019 Forecast United States Total Personal Computing Devices, Market Penetration, Percent of Households & Businesses United States Consumer Personal Computing Devices, Market Penetration, Percent of Households

5 United States Enterprise Personal Computing Devices, Market Penetration Percent of Businesses United States Personal Communications Device Market: Penetration, Percent of Households & Businesses United States Personal Devices TAM Penetration 2019 and 2023 Density Device Density - PCs and Tablets per Person and Employee United States Total Personal Computing Devices, Density (Devices per Penetrated Household or Business) United States Consumer Personal Computing Devices, Density (Devices per Penetrated Household) United States Enterprise Personal Computing Devices, Density (Devices per Penetrated Business) United States Personal Communications Devices, Density (Devices per Penetrated Household or Business) United States Personal Devices TAM Density 2019 and 2023 Replacement Rates Total Personal Devices Unit Shipments CAGR by Replacement Rate CAGR United States Consumer Desktop, Percent of Installed Base Units by Year Purchased United States Consumer Desktop, Time in Use Metrics Replacement Cycle Length United States Total Personal Computing Devices, Replacement Cycle Length (Y) United States Consumer Personal Computing Devices, Replacement Cycle Length (Y) United States Enterprise Personal Computing Devices, Replacement Cycle Length (Y) United States Personal Communications Device Market: Replacement Cycle Length United States Personal Devices Replacement Cycle Length 2019 and 2023 Age of Retired Units United States Total Personal Computing Devices, Age of Retired Units (Y) United States Consumer Personal Computing Devices, Age of Retired Units (Y)

6 United States Enterprise Personal Computing Devices, Age of Retired Units (Y) United States Personal Communications Device Market: Age of Retired Units (Y) United States Personal Devices Removal Age 2019 and 2023 Purpose and Location United States Consumer Personal Device (by Location and Primary Purpose) Unit Shipments (K) United States Enterprise Personal Device (by Location and Primary Purpose) Unit Shipments (K) United States Consumer Personal Device (by Location and Primary Purpose) Installed Base (K) United States Enterprise Personal Device (by Location and Primary Purpose) Installed Base (K) United States Personal Devices 2019 Unit Shipments Annual Growth Rate - Locations and Primary Purpose United States Personal Devices Unit Shipments CAGR - Locations and Primary Purpose United States Personal Computing Devices, Percent of Unit Shipments, 2019 and Locations and Primary Purpose United States Personal Devices 2019 Installed Base Annual Growth Rate - Locations and Primary Purpose United States Personal Devices Installed Base CAGR - Locations and Primary Purpose United States Personal Computing Devices, Percent of Installed Base, 2019 and Locations and Primary Purpose United States Personal Devices TAM Penetration 2019 and Locations and Primary Purpose United States Personal Devices TAM Density 2019 and Locations and Primary Purpose United States Personal Devices Removal Age 2019 and Locations and Primary Purpose United States Personal Devices Replacement Cycle Length 2019 and Locations and Primary Purpose Hybrids United States Consumer Convertible Mobile PCs Percent of Total Mobile PCs United States Enterprise Convertible Mobile PCs Percent of Total Mobile PCs Hybrid PCs Unit Shipments % of Mobile PCs & Tablets Hybrid PCs Installed Base % of Mobile PCs & Tablets Mobile PCs Unit Shipments % of Hybrid PCs Mobile PCs Installed Base % of Hybrid PCs

7 Market Overview Unit Shipments of Personal Computing and Communication Devices; PCs, Tablets, and Mobile Phones, in the United States will be essentially flat over the next five years. Notwithstanding an expected -4.4% decline in 2019, the rest of the forecast period will produce annual growth rates ranging from 1.0% in 2020 and rising to 4.8% by 2023, resulting in a Compound Annual Growth Rate of 1.4%. We expect Replacement Rates for most products to continue slow through 2021, finally begin to accelerate starting in 2022 as compelling new replacement product are introduced, failure rates due to age reach critical levels, and both existing and emerging Use-Case requirements can no longer met by existing product. Mobile PCs will continue to be the favored form factor as Desktop PCs penetration continues to decrease approaching core floor levels in both Consumer and Enterprise Sectors, and Tablet penetration continues to slow approaching theoretical maximum levels, as Use-Cases, costs, and ergonomics favor Mobile PCs. While the Consumer Sector Unit Shipment growth will produce a CAGR of +2.4%, the decline in growth for Desktop PCs, Tablets, and Mobile Phones will not offset Mobile PC growth in the Enterprise Sector resulting in a -3.0% CAGR. Forecasting Approach and Process In order for the readers and users of this forecast report to have confidence in its presented results it is necessary to understand the forecasting approach, process, and methodologies employed. Our process has five steps. 1. Top-Down Density and Penetration Analysis of long-term trends. These analyses are presents in these charts Device Density - PCs and Tablets per Person and Employee United States Personal Computing Device Market Penetration, , April 2019 Forecast 2. Top-Down forecasts for each major product 3. Consumer and Enterprise forecasts for each product Base forecasts for Products without Form Factors 4. Form Factor forecasts for each product in each segment Base forecasts for Products with Form Factors 5. Bottoms-Up Aggregation and Roll-Ups from the Base forecasts including aggregating to the alternative Purpose and Location taxonomy.

8 Each step the forecasting process begins by analyzing historical trends in four key causal influencing factors; 1. Total Available Market (TAM) the number of Households and Business in the US economy. This is obtained from the Daniel Research Group Business Economic Demographic Forecast. 2. Penetration Levels The percent of those Households and/or Business that own and use the device. These follow logistic S-Curves for both growth and declining products. Analysis of causal factors influencing future buyer decisions determine to what degree the function parameters need to be adjusted. 3. Density the average number of devices in use in those penetrated Households and/or Businesses For the most part these follow linear or growth trends and tend to decrease as penetration increases. However, they are very much dependent on product, segment, growth phase, and user behavior context. For example, products in the declining phases of their life cycle will often exhibit increasing density as penetration decreases, as the remaining TAM units are more likely to be dependent on the product and are multiple unit users. In emerging product markets, density is dependent on the timing of subsequent/multiple purchases. In some case early adopter are more likely to be multiple unit buyers at the time of first purchase than later adopters. In other case the early adopters, while still more likely to purchase additional units, will do so at a later date. Other patterns are also possible 4. Replacement Rates the rate at which the device is replaced. This behavior can also be context dependent. For example, when a new replacement product is introduced, the users most likely to replace may be those with the oldest units, those with the most recently purchased units, or in-between. Most user populations are not homogeneous with respect to propensity to replace in terms of age. How long are current users expected to continue to use their current device until they replacement them? - is the central question that device vendors and sellers what to know, and very difficult to answer. Asking current users when they expect to replace requires them to have knowledge of future economic and market conditions that they can not reasonably know. The Daniel Research Groups EQS methodology and models utilize four different metrics to measure historical and forecasted device usage time. a. Retention Rate Distribution Mean (RRD-µ), Standard Deviation and Maximum Life. These are inputs to model that are based on our analysis of economic, market, and user behavior factors. It is not an output of the models. b. Average Installed Base Age (AIBA). The EQS models compute the age distribution of the installed base in every year allowing for the computation of this

9 metric. However, it is often is highly dependent on the relative magnitude of current unit shipments in relationship to the installed base, and is therefore not an accurate estimate of how long users will continue to use the device. While the AIBA is still computed by the EQS models, we have decided not to include it in output tables and charts in this report. c. Replacement Cycle Length (RCL). This is the length of time it will take for all of the existing units in the installed base to be replaced given the current installed base size, unit shipments, and number of units removed from the installed base in that year. The EQS algorithm allows the RRD-µ to be adjusted to produce a target RCL value. Therefore, the models may be configured to use RCL as either an input or an output variable on an ad hoc basis. d. Average Removal Age (ARA) This is the average age of the units removed/retired for any reason from the installed base. It is an estimate of the average age that would be computed if you could ask every user who stopped using the device, how long they had used it. This is a new output metric from the EQS models and is include in the tables and charts in this report. ARA is highly correlated with RCL and the combination of the two is a good estimate of the true expected in use life. Differences between the two reflect difference in the user population replacement behavior related to unit age. The value of each of these metrics is in the trend more than in then point values. An example of the installed base age distribution is presented in this chart. United States Consumer Desktop, Percent of Installed Base Units by Year Purchased A comparison of the four installed base age metrics is presented in this chart. United States Consumer Desktop, Time in Use Metrics While we do consider trends in Unit Shipments necessary to establish historical context, we view Unit Shipments to be a result, not a cause, and therefore contain little or no predictive properties. When considering trends in the key influencing factors, we always ask the following key questions; Is the process that produced the historical results the same as will produce the future result. In many cases the answer is no. Causal influencing factors operating in the past often are no longer relevant or even exist. Likewise, new causal influencing factors are emerging. Therefore, the parameters governing the expression of these trends in mathematical terms in our forecast models are adjusted to reflect the changes in the causal influencing factors. In order to facilitate this process, it is necessary to understand the long-term trends and pattern of both the input and output metrics, as well as the causal influences. Many of the following sections presenting our forecasts and analysis will include Long-Term charts that establish context.

10 Our analysis of the key influencing causal factors concluded that very little will change over the next five years relative to the recent past. Therefore, our overall forecast predicts a fairly stable market for most Personal Computing and Communication Devices producing moderate growth. While there will be some slight change to the both the magnitude and structure of the Household and Business TAMs, Penetration Rates will continue their historic trends in most product cases, as will Densities. The factor that will have the most possible variance on the range of possible forecast outcomes is the rate that users will or will not replace their PCs, Tablets, and Mobile Phones with newer offerings. Changes to assumptions about TAM, Penetration, and Density will have, for the most part, proportional changes to Unit Shipments. Changes to Replacement Rate assumptions can have significantly more weight on Unit Shipment Forecasts. Forecast assumptions about all of the primary variables are derived from quantitative and qualitative assessments about the economy, product introductions, or lack of, as well as changing Consumer and Enterprise Use Cases and user/buyer behaviors. While TAM, Penetration, and Density carry some inertia in that they are slow moving and non-volatile time-series, Replacement Rates can change relatively quicker. However, given our current understanding of all of the causal influences, we do not see much change to Replacement Rates other than those tied to changing economic conditions. Alternative Taxonomy DRG has found it useful to aggregate the base models into a taxonomy based on Location - Fixed or Mobile, and Primary Purpose Content Creation and/or Capture, Delivery, or Communication. Fixed Creation Desktop PCs Mobile Delivery Slate Tablets and e-readers Mobile Creation & Capture Mobile PCs and Detachable Tablets Communication Mobile Phones

11 Market Tables

12

13

14 Next Five Years Over the Next Five Years: Personal Computers and Tablets 532 million new PCs and Tablets will be purchased by Households and Businesses 96.8% will be replacements for older Personal Computing Devices 6 million Households and Businesses will buy a PC or Tablet for the first time The average number of Personal Computing Devices per Business will remain essentially unchanged at 30.3 devices per Business, while the average number of Personal Computing Devices per Households will also remain essentially unchanged to 2.45 devices per Household. The time required to replace all of the installed Personal Computing Devices will remain essentially constant at 5.9 years. Over the Next Five Years: Mobile Phones Million Mobile Phones will be purchased 97.9% will be replacements for older Mobile Phones 9.2 million Households will buy a Mobile Phone for the first time bringing the Household penetration to 97.7% The average number of Smartphones per Household will decrease slightly to 2.38 per Household by 2023 The time required to replace all of the Mobile Phones will remain unchanged at 34.3 Months

15 Major Causal Influences and Trends The United States Economy The economy has an obvious and direct influence on technology user buying behavior. Economic growth encourages buying, economic stagnation or decline inhibits buying. Our models express our assessment of forecasted economic growth in the annual growth rate patterns we apply to both the Unit Shipments and the Replacement Cycle Length inputs. We construct these patterns based on our analysis of economic forecast for GDP and Employment Growth from a number of credible US governments and international sources, primarily the Congressional Budget Office. Notwithstanding any unforeseen economic shocks or adverse effects from tariff or monetary policy decisions, the economy is expected to show growth over the forecast period, although at a declining rate according to the CBO. DRG also develops its own US Business Economic Demographic Forecast that reflect not just the CBO economic forecasts, but forecasts at the Industry by Size Class level derived form other sources including the Census Bureau and the Bureau of Labor Statistics

measured as number of businesses.")

16 Our economic forecast projects not just overall growth, but changes to the Business Economic Demographic Structure of the US economy that directly effects our estimates of the Enterprise Total Available Market (TAM) measured as number of businesses. Over the forecast period, while very small business will show growth, the number of small business in the 5 to 9, and 10 to 19 size classes will decline, as will the number of employees in those size classes. The losses will be absorbed by the larger size classes. This will have significant influence on demand for products targeted by size class.

17

18 Please contact Daniel Research Group to obtain our 78-page detailed US Business Economic Demographic Forecast.

19 Unit Shipments

20

21

22

23

24

25

26 Installed Base

27

28

29

30

31

32

33 Penetration

34

35

36

37

38

39 Density

40

41

42

43

44

45 Replacement Rates

46

47 Replacement Cycle Length

48

49

50

51

52 Average Removal Age

53

54

55

56

57 Purpose and Location

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73 Hyprid PC 2-in-1

74

75

76

77 Product Forecast Tables

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103 Sources of Historical Data Historical data was obtained from the following of available sources including press releases, published reports and presentations, and publicly available databases. Device or Metric Desktop PCs Mobile PCs Unit Shipments Environmental Protection Agency IDC Environmental Protection Agency IDC Installed Base/Penetration Computer Almanac etforecaster International Telecommunications Union Worldbank Computer Almanac etforecaster International Telecommunications Union Worldbank Tablets IDC Pew Research Center Mobile Phones Households Businesses Consumer Technology Association Telecommunications Industry Association US Census Bureau Bureau of Economic Analysis Bureau of Labor Statistics Congressional Budget Office Department of Defense US Census Bureau US Office of Personal Management Cellular Telephone Industries Association Centers for Disease Control and Prevention GSMA International Telecommunications Union Organization for Economic Co-operation and Development Telecommunications Industry Association Worldbank

104 Data obtained from a variety of sources, often using different definition and methodologies, are frequently inconsistent with each other. DRG employs the EquilibriumSolver to identify and correct these differences, and produce historic time-series of Unit Shipments, Installed Bases, Replacement Rates, Average Ages, Densities and Penetration Rates that are internally consistent with each other, and correlate highly with external quantitative data and qualitative data criteria. DRG believes the resulting historical baseline is the most accurate complete accounting of the US Personal Device Market from its inception in 1975

105 Methodology The DRG Forecasting Approach In order to understand our forecast conclusions, a review of our forecast approach is necessary. Although forecasts of Unit Shipments and Revenues are of most interest to our clients, we consider these to be output results with very little predictive properties in and of themselves. Rather, we base our forecasts on understanding the trends, and the influences on those trends, of the following primary causal variables. Total Available Market (TAM) The number of potential buyers in the consumer and/or enterprise segments Penetration The percent of buyers, households and/or businesses, that has or will purchase the product or service. Density the number of product or service units in uses per penetrated household and/or business. Replacement Rate rate at which users are replacing older units with new ones. This is primarily measured in terms of the Replacement Cycle Length. The length of time it would take to replace all of the current units in the installed base given the current rate of new unit shipments and the rate of old unit replacement. Our forecast approach proceeds in four steps 1. Penetration There are Top-Down Long-Term models that forecast future market penetration of the primary major products categories based on long-terms historical trends. 2. Top-Down The primary major products are split by segment (consumer and enterprise) and form factor, as needed. 3. Base Each individual product/segment/form factor forecasts in adjusted to reflect our analysis of the economic, demographic, technological, market and user behavior influencing factors. 4. Bottom-Up, Roll-Up The base forecasts are roll-up to higher levels and other aggregations. While some of the output metrics such as Unit Shipments, Revenues and Installed Bases are additive, other such as Density, Penetration, Replacement Cycle Length, and Installed Base Age or not can only be computed using DRG s proprietary EQS methodology. Models are neat, but markets are messy. Any market model is at best an idealized simplistic version of the a complex real world process. How useful any model can be is a function of how well it encapsulates the basic causal relationships that drive cause and effect. EQS is a demand side causal model. It does not directly include any supply side trends or influences other than how they effect the demand side causal variables or indirectly, the effects and derivatives.

the percent of the TAM that has purchased and is using the product or service 3.")

106 Ultimately, the demand for products and services is a function of only four independent variables. 1. TAM Total Available (or Addressable) Market meausred as puchasing/using units 2. Penetration (Percent) the percent of the TAM that has purchased and is using the product or service 3. Density The average number of units purchased and in use by the TAM units that have purchased and are using the product or service 4. Replacement (Rate) The rate at which the penetrated TAM replace product or service units. In the EQS model the Replacement is measured by the Replacement Cycle Length (RCL) metric When EQS models a Causal Flow, these four inputs compute the primary effect outputs; Unit Shipments and Insalled Base, as well as the derivative metrics, Annual Growth Rats, CAGRs, and the Installed Base Average Age. For example, an increase in the penetration rate will result in an increase in unit shipments and/or an increase in the installed base, as well as changing the derivative metrics. When EQS models a Counter Causal Flow, the logic flows in the other direction. An increase in the Unit Shipments will require an increase in one or more of the Causal variables, as well as changing the derivative metrics. The strength of EQS as a market modeling and forecasting tool derives from two attributes; 1. The ability to run both Causal and Counter Causal logic 2. A closed system of relationships that can only produce outputs that meet real world constraints and criteria set by the user

107 Total Available Market (TAM) The TAM used in the Mobile Phone, and Consumer Desktop, Mobile, and Tablet PC models is Households. The historic data was obtained from the United States Census Bureau and projected to 2026 by DRG. The TAM used in the Enterprise Desktop, Mobile, and Tablet PC models is Primary Firms from the DRG Business Demographic Baseline and Forecast. Primary Firms represent the count of Business in the total US Economy, both Private and Public Sector that are categorized by their primary business. The DRG Business Demographic Baseline and Forecast is a database of United States Firms, Primary Firms, Establishments, and Payrolls by Private and Public Sectors, by 2-Digit NAICS industries, from 1998 to It is derived from data obtained from the US Census Bureau, The Bureau of Economic Analysis, the Bureau of Labor Statistics, The Department of Defense, and the Congressional Budget Office Forecast Updates DRG will update these forecasts periodically as actual year-to-date results become available. Utilizing the DRG ProjectionSolver algorithm, new current year projections based on historic trended quarterly or monthly patterns are computed. Based on these projections, adjustments may be made to the primary EQS models

108 About Daniel Research Group Daniel Research Group is a market research and consulting firm servicing technology clients. Our primary focus is developing custom market models and forecasts. We support clients three ways. 1. We work independently or collaboratively with the client s own analysts to produce custom technology product/service market models and forecasts. 2. We work collaboratively with the client s own analysts to design and develop the modeling applications that they will use to develop their own market models and forecasts. 3. We train client s analysts in the theory and practice of technology market modeling and forecasting. Most of our work utilizes the inventory of proprietary methodologies and algorithms that we have developed over more than 30 years. We have built technology forecasting market models for many major technology vendors, market research firms, and industry organizations. While our core competency is forecasting, our subject experience covers the entire technology and technology-enabled product/service landscape. We also support our engagements with traditional qualitative and quantitative research, as well as tactical and strategic consulting services. Stephen J. Daniel - President With three decades in the Information Technology Industry, Mr. Daniel has developed a unique blend of Market and Technology experience coupled with a deep understanding of Market Research Methodology. His primary strength is in understanding the decision-making context within which the results of his research will be applied. This is manifested by his ability to design and execute studies that precisely meet client objectives in a timely fashion and at reasonable costs. Mr. Daniel received his BS in Finance from Northeastern University and earned an MBA in Quantitative Analysis from New York University. He is a member of the American Statistical Association, The Market Research Association of America, the American Marketing Association and the Qualitative Research Association of America. Contact Information Steve@DanielRG.com (617)

United States Computing and Telecommunications Personal Device Market Forecast: Q Update

United States Computing and Telecommunications Personal Device Market Forecast: 2018-2022 Q4 2017 Update Table of Contents List of Tables List of Charts Market Overview Causal Influences and Trends o Functional

United States Computing and Telecommunications Personal Device Market Forecast: 2018-2022 Q4 2017 Update Table of Contents List of Tables List of Charts Market Overview Causal Influences and Trends o Functional

emarketer US Social Network Usage StatPack

May 2016 emarketer US Social Network Usage StatPack Presented by Learning from Social Advertising Data Trends Video Views ONCE A USER WATCHES 25% OF A VIDEO, DO THEY Stop Watching Watch 50% Watch 75% Finish

May 2016 emarketer US Social Network Usage StatPack Presented by Learning from Social Advertising Data Trends Video Views ONCE A USER WATCHES 25% OF A VIDEO, DO THEY Stop Watching Watch 50% Watch 75% Finish

TELECOMS SERVICES FOR SMALL AND MEDIUM-SIZED ENTERPRISES: WORLDWIDE FORECAST

RESEARCH FORECAST REPORT TELECOMS SERVICES FOR SMALL AND MEDIUM-SIZED ENTERPRISES: WORLDWIDE FORECAST 2017 2022 CATHERINE HAMMOND analysysmason.com About this report This report analyses the demand for

RESEARCH FORECAST REPORT TELECOMS SERVICES FOR SMALL AND MEDIUM-SIZED ENTERPRISES: WORLDWIDE FORECAST 2017 2022 CATHERINE HAMMOND analysysmason.com About this report This report analyses the demand for

Socioeconomic Overview of Ohio

2 Socioeconomic Overview of Ohio Introduction The magnitude of the economic impact of Ohio s airports is linked to the demand that is generated within the state for aviation goods and services. As population,

2 Socioeconomic Overview of Ohio Introduction The magnitude of the economic impact of Ohio s airports is linked to the demand that is generated within the state for aviation goods and services. As population,

Economic Update. Automotive Insights Conference. Paul Traub. Federal Reserve Bank of Chicago January 18, Senior Business Economist

Economic Update Automotive Insights Conference Federal Reserve Bank of Chicago January 18, 2018 Paul Traub Senior Business Economist Main Economic Indicators Year-over-year Comparison 2015 2016 2017 GDP

Economic Update Automotive Insights Conference Federal Reserve Bank of Chicago January 18, 2018 Paul Traub Senior Business Economist Main Economic Indicators Year-over-year Comparison 2015 2016 2017 GDP

IDC MarketScape: Worldwide Cloud Professional Services 2018 Vendor Assessment

IDC MarketScape IDC MarketScape: Worldwide Cloud Professional Services 2018 Vendor Assessment Gard Little Chad Huston THIS IDC MARKETSCAPE EXCERPT FEATURES DELL EMC IDC MARKETSCAPE FIGURE FIGURE 1 IDC

IDC MarketScape IDC MarketScape: Worldwide Cloud Professional Services 2018 Vendor Assessment Gard Little Chad Huston THIS IDC MARKETSCAPE EXCERPT FEATURES DELL EMC IDC MARKETSCAPE FIGURE FIGURE 1 IDC

Cloud Going Mainstream All Are Trying, Some Are Benefiting; Few Are Maximizing Value

All Are Trying, Some Are Benefiting; Few Are Maximizing Value Latin America Findings September 2016 Executive Summary Cloud adoption has increased 49% from last year, with 78% of companies in Latin America

All Are Trying, Some Are Benefiting; Few Are Maximizing Value Latin America Findings September 2016 Executive Summary Cloud adoption has increased 49% from last year, with 78% of companies in Latin America

MAIL DIVERSION. This paper focuses primarily on the forecasted impact of technology on postal volumes

MAIL DIVERSION Mail volumes are under attack from a number of sources: technological diversion, the economy, competition, regulatory changes, business consolidation and other factors. This paper focuses

MAIL DIVERSION Mail volumes are under attack from a number of sources: technological diversion, the economy, competition, regulatory changes, business consolidation and other factors. This paper focuses

IDC MarketScape: Worldwide Datacenter Transformation Consulting and Implementation Services 2016 Vendor Assessment

IDC MarketScape IDC MarketScape: Worldwide Datacenter Transformation Consulting and Implementation Services 2016 Vendor Assessment Chad Huston Ali Zaidi THIS IDC MARKETSCAPE EXCERPT FEATURES: WIPRO IDC

IDC MarketScape IDC MarketScape: Worldwide Datacenter Transformation Consulting and Implementation Services 2016 Vendor Assessment Chad Huston Ali Zaidi THIS IDC MARKETSCAPE EXCERPT FEATURES: WIPRO IDC

Economic Update German American Chamber of Commerce

Economic Update German American Chamber of Commerce Federal Reserve Bank of Chicago October 6, 2015 Paul Traub Senior Business Economist U.S. Real GDP Billions Chained $2009, % Change Q/Q at SAAR $ Billions

Economic Update German American Chamber of Commerce Federal Reserve Bank of Chicago October 6, 2015 Paul Traub Senior Business Economist U.S. Real GDP Billions Chained $2009, % Change Q/Q at SAAR $ Billions

IDC MarketScape: Worldwide Cloud Professional Services 2014 Vendor Analysis

IDC MarketScape IDC MarketScape: Worldwide Cloud Professional Services 2014 Vendor Analysis Gard Little Chad Huston THIS IDC MARKETSCAPE EXCERPT FEATURES: CISCO IDC MARKETSCAPE FIGURE FIGURE 1 IDC MarketScape

IDC MarketScape IDC MarketScape: Worldwide Cloud Professional Services 2014 Vendor Analysis Gard Little Chad Huston THIS IDC MARKETSCAPE EXCERPT FEATURES: CISCO IDC MARKETSCAPE FIGURE FIGURE 1 IDC MarketScape

IDC MarketScape: Worldwide Network Consulting Services 2017 Vendor Assessment

IDC MarketScape IDC MarketScape: Worldwide Network Consulting Services 2017 Vendor Assessment Leslie Rosenberg THIS IDC MARKETSCAPE EXCERPT FEATURES: CISCO IDC MARKETSCAPE FIGURE FIGURE 1 IDC MarketScape

IDC MarketScape IDC MarketScape: Worldwide Network Consulting Services 2017 Vendor Assessment Leslie Rosenberg THIS IDC MARKETSCAPE EXCERPT FEATURES: CISCO IDC MARKETSCAPE FIGURE FIGURE 1 IDC MarketScape

Global Headquarters: 5 Speen Street Framingham, MA USA P F

Global Headquarters: 5 Speen Street Framingham, MA 01701 USA P.508.872.8200 F.508.935.4015 www.idc.com C O M P E T I T I V E A N A L Y S I S I D C M a r k e t S c a p e : W o r l d w i d e D a t a c e

Global Headquarters: 5 Speen Street Framingham, MA 01701 USA P.508.872.8200 F.508.935.4015 www.idc.com C O M P E T I T I V E A N A L Y S I S I D C M a r k e t S c a p e : W o r l d w i d e D a t a c e

Open Source Cloud Platforms: OpenStack

Open Source Cloud Platforms: OpenStack This Market Monitor overview report on the OpenStack marketplace provides updated vendor estimates through Q2 2017. OpenStack, the open source cloud project, was

Open Source Cloud Platforms: OpenStack This Market Monitor overview report on the OpenStack marketplace provides updated vendor estimates through Q2 2017. OpenStack, the open source cloud project, was

Cloud Going Mainstream All Are Trying, Some Are Benefiting; Few Are Maximizing Value. An IDC InfoBrief, sponsored by Cisco September 2016

All Are Trying, Some Are Benefiting; Few Are Maximizing Value September 2016 Executive Summary Cloud adoption has increased 61% from last year, with 73% pursuing a hybrid cloud strategy and on-premises

All Are Trying, Some Are Benefiting; Few Are Maximizing Value September 2016 Executive Summary Cloud adoption has increased 61% from last year, with 73% pursuing a hybrid cloud strategy and on-premises

DBMS Software Market Forecast, (Executive Summary) Executive Summary

Executive Summary") DBMS Software Market Forecast, 2003-2007 (Executive Summary) Executive Summary Publication Date: 4 September 2003 Author Colleen Graham This document has been published to the following Marketplace codes:

DBMS Software Market Forecast, 2003-2007 (Executive Summary) Executive Summary Publication Date: 4 September 2003 Author Colleen Graham This document has been published to the following Marketplace codes:

The U.S. Manufacturing Extension Partnership - MEP

The U.S. Manufacturing Extension Partnership - MEP Roger D. Kilmer Director, MEP National Institute of Standards and Technology (NIST) U.S. Department of Commerce roger.kilmer@nist.gov 301-975-5020 http://www.nist.gov/mep/

The U.S. Manufacturing Extension Partnership - MEP Roger D. Kilmer Director, MEP National Institute of Standards and Technology (NIST) U.S. Department of Commerce roger.kilmer@nist.gov 301-975-5020 http://www.nist.gov/mep/

Magento: A Year in Review

Magento: A Year in Review Magento Presents: Community Insights Brought to you by: Magento is proud to present Community Insights to help merchants develop strategies and tactics to better serve their customers.

Magento: A Year in Review Magento Presents: Community Insights Brought to you by: Magento is proud to present Community Insights to help merchants develop strategies and tactics to better serve their customers.

The Role of the Federal Reserve Metropolitan Research Group UM-D

The Role of the Federal Reserve Metropolitan Research Group UM-D Federal Reserve Bank of Chicago January 24, 2017 Paul Traub Senior Business Economist The Federal Reserve System 1 Functions of the Federal

The Role of the Federal Reserve Metropolitan Research Group UM-D Federal Reserve Bank of Chicago January 24, 2017 Paul Traub Senior Business Economist The Federal Reserve System 1 Functions of the Federal

Trends in Fixed Public Network Services: Austria, (Executive Summary) Executive Summary

Executive Summary") Trends in Fixed Public Network Services: Austria, 2000-2006 (Executive Summary) Executive Summary Publication Date: September 25, 2002 Authors Michal Halama Maureen Coulter Katja Ruud Susan Richardson

Trends in Fixed Public Network Services: Austria, 2000-2006 (Executive Summary) Executive Summary Publication Date: September 25, 2002 Authors Michal Halama Maureen Coulter Katja Ruud Susan Richardson

Global Semiconductor Dry Strip Systems Market

Global Semiconductor Dry Strip Systems Market 2014-2018 Global Semiconductor Dry Strip Systems Market 2014-2018 Sector Publishing Intelligence Limited (SPi) has been marketing business and market research

Global Semiconductor Dry Strip Systems Market 2014-2018 Global Semiconductor Dry Strip Systems Market 2014-2018 Sector Publishing Intelligence Limited (SPi) has been marketing business and market research

Cloud Going Mainstream All Are Trying, Some Are Benefiting; Few Are Maximizing Value

All Are Trying, Some Are Benefiting; Few Are Maximizing Value Germany Findings September 2016 Executive Summary Cloud adoption has increased 70% from last year, with 71% of companies in Germany pursuing

All Are Trying, Some Are Benefiting; Few Are Maximizing Value Germany Findings September 2016 Executive Summary Cloud adoption has increased 70% from last year, with 71% of companies in Germany pursuing

Don t Get Left Behind

August 2015 Executive Summary Cloud adoption is growing, but relatively few organizations have advanced cloud strategies Achieving greater levels of cloud adoption allows organizations to materially improve

August 2015 Executive Summary Cloud adoption is growing, but relatively few organizations have advanced cloud strategies Achieving greater levels of cloud adoption allows organizations to materially improve

Light Vehicle Sales Are We at a Turning Point?

Light Vehicle Sales Are We at a Turning Point? Federal Reserve Bank of Chicago June 3, 2016 Paul Traub Senior Business Economist Overview U.S. Economy (C + I + G + Nx) U.S. Consumer Ability and Willingness

Light Vehicle Sales Are We at a Turning Point? Federal Reserve Bank of Chicago June 3, 2016 Paul Traub Senior Business Economist Overview U.S. Economy (C + I + G + Nx) U.S. Consumer Ability and Willingness

Mobile Communication Device Contract Consolidation for State Agencies. Report to the Joint Legislative Oversight Committee on Information Technology

Mobile Communication Device Contract Consolidation for State Agencies Report to the Joint Legislative Oversight Committee on Information Technology Chris Estes State Chief Information Officer November

Mobile Communication Device Contract Consolidation for State Agencies Report to the Joint Legislative Oversight Committee on Information Technology Chris Estes State Chief Information Officer November

Water Asset Management Conference. Convergence of Water and Data Launches Wave of New Opportunities and Solutions. Boston, MA.

Convergence of Water and Data Launches Wave of New Opportunities and Solutions Boston, MA October 2017 WWW.BLUEFIELDRESEARCH.COM water INSIGHT Bluefield Research is an independent advisory firm positioned

Convergence of Water and Data Launches Wave of New Opportunities and Solutions Boston, MA October 2017 WWW.BLUEFIELDRESEARCH.COM water INSIGHT Bluefield Research is an independent advisory firm positioned

WIRELESS NETWORK DATA TRAFFIC: WORLDWIDE TRENDS AND FORECASTS

RESEARCH FORECAST REPORT WIRELESS NETWORK DATA TRAFFIC: WORLDWIDE TRENDS AND FORECASTS 2016 2021 STEPHEN WILSON Analysys Mason Limited 2017 analysysmason.com About this report This report presents 5-year

RESEARCH FORECAST REPORT WIRELESS NETWORK DATA TRAFFIC: WORLDWIDE TRENDS AND FORECASTS 2016 2021 STEPHEN WILSON Analysys Mason Limited 2017 analysysmason.com About this report This report presents 5-year

State of the Satellite Industry Report

State of the Satellite Industry Report August 2011 Sponsored by the Prepared by Futron Corporation SIA Member Companies as of August 2011 2 Study Overview The SIA s 14 th annual comprehensive study of

State of the Satellite Industry Report August 2011 Sponsored by the Prepared by Futron Corporation SIA Member Companies as of August 2011 2 Study Overview The SIA s 14 th annual comprehensive study of

RED HAT ENTERPRISE LINUX. STANDARDIZE & SAVE.

RED HAT ENTERPRISE LINUX. STANDARDIZE & SAVE. Is putting Contact us INTRODUCTION You know the headaches of managing an infrastructure that is stretched to its limit. Too little staff. Too many users. Not

RED HAT ENTERPRISE LINUX. STANDARDIZE & SAVE. Is putting Contact us INTRODUCTION You know the headaches of managing an infrastructure that is stretched to its limit. Too little staff. Too many users. Not

SIP Global Market 7-Year Forecast and Analysis. Table of Contents. EasternManagementGroup 0

2018-2024 SIP Global Market 7-Year Forecast and Analysis Table of Contents EasternManagementGroup 0 2018 The Eastern Management Group, Inc. EasternManagementGroup 1 Introduction 2018-2024 SIP Global Market

2018-2024 SIP Global Market 7-Year Forecast and Analysis Table of Contents EasternManagementGroup 0 2018 The Eastern Management Group, Inc. EasternManagementGroup 1 Introduction 2018-2024 SIP Global Market

T-Mobile US Q4 and Full Year 2013

T-Mobile US Q4 and Full Year 2013 Disclaimer This presentation contains forward-looking statements within the meaning of the U.S. federal securities laws. For those statements, we claim the protection

T-Mobile US Q4 and Full Year 2013 Disclaimer This presentation contains forward-looking statements within the meaning of the U.S. federal securities laws. For those statements, we claim the protection

Tieto in Russia. Capital Market Day 25 November 2010 Helsinki, Finland. Tuomo Summanen Country Manager, Tieto Russia Tieto Corporation

Tieto in Russia Capital Market Day 25 November 2010 Helsinki, Finland Tuomo Summanen Country Manager, Tieto Russia Content Economic trends Russian IT services market Tieto s current business in Russia

Tieto in Russia Capital Market Day 25 November 2010 Helsinki, Finland Tuomo Summanen Country Manager, Tieto Russia Content Economic trends Russian IT services market Tieto s current business in Russia

IAB Ad Unit Guidelines 2009 Update

IAB Ad Unit Guidelines 2009 Update Released November 2009 This document has been developed by the IAB s Reimagining Interactive Advertising Taskforce and reviewed by the IAB s Ad Ops and Sales Executive

IAB Ad Unit Guidelines 2009 Update Released November 2009 This document has been developed by the IAB s Reimagining Interactive Advertising Taskforce and reviewed by the IAB s Ad Ops and Sales Executive

Vertical Market Trends: Western Europe, (Executive Summary) Executive Summary

Executive Summary") Vertical Market Trends: Western Europe, (Executive Summary) Executive Summary Publication Date: 21 March 2003 Authors Cathy Tornbohm Peter Redshaw This document has been published to the following Marketplace

Vertical Market Trends: Western Europe, (Executive Summary) Executive Summary Publication Date: 21 March 2003 Authors Cathy Tornbohm Peter Redshaw This document has been published to the following Marketplace

Connected & Smart Home Research Package

TECHNOLOGY, MEDIA & TELECOMMUNICATION KEY COMPONENTS Intelligence Services Real-time access to continually updated market data and forecasts, analyst insights, topical research reports and analyst presentations.

TECHNOLOGY, MEDIA & TELECOMMUNICATION KEY COMPONENTS Intelligence Services Real-time access to continually updated market data and forecasts, analyst insights, topical research reports and analyst presentations.

Competency Definition

Adult Children's Outreach Technical Teen Acquisition Adaptability The ability to effectively process library material orders; knowledge of vendor software, processes, products, and updates x x The ability

Adult Children's Outreach Technical Teen Acquisition Adaptability The ability to effectively process library material orders; knowledge of vendor software, processes, products, and updates x x The ability

Open Source Cloud Platforms: OpenStack

Open Source Cloud Platforms: OpenStack This Market Monitor overview report on the OpenStack marketplace provides updated vendor estimates through Q3 2016. OpenStack, the open source cloud project, was

Open Source Cloud Platforms: OpenStack This Market Monitor overview report on the OpenStack marketplace provides updated vendor estimates through Q3 2016. OpenStack, the open source cloud project, was

The future of UC&C on mobile

SURVEY REPORT The future of UC&C on mobile Published by 2018 Introduction The future of UC&C on mobile report gives us insight into how operators and manufacturers around the world rate their unified communication

SURVEY REPORT The future of UC&C on mobile Published by 2018 Introduction The future of UC&C on mobile report gives us insight into how operators and manufacturers around the world rate their unified communication

IDC MarketScape: Worldwide Datacenter Transformation Consulting and Implementation Services 2014 Vendor Assessment

IDC MarketScape IDC MarketScape: Worldwide Datacenter Transformation Consulting and Implementation Services 2014 Vendor Assessment Ali Zaidi Gard Little THIS IDC MARKETSCAPE EXCERPT FEATURES: HCL IDC MARKETSCAPE

IDC MarketScape IDC MarketScape: Worldwide Datacenter Transformation Consulting and Implementation Services 2014 Vendor Assessment Ali Zaidi Gard Little THIS IDC MARKETSCAPE EXCERPT FEATURES: HCL IDC MARKETSCAPE

Solutions for Rising Video Surveillance Storage Demands

IHS TECHNOLOGY FEBRUARY 2016 Solutions for Rising Video Surveillance Storage Demands Josh Woodhouse, Senior Analyst, Video Surveillance TABLE OF CONTENTS The Video Surveillance Market... 2 Options and

IHS TECHNOLOGY FEBRUARY 2016 Solutions for Rising Video Surveillance Storage Demands Josh Woodhouse, Senior Analyst, Video Surveillance TABLE OF CONTENTS The Video Surveillance Market... 2 Options and

Economic Update Baker College - Flint

Economic Update Baker College - Flint Federal Reserve Bank of Chicago January 10, 2017 Paul Traub Senior Business Economist Main Economic Indicators Year-over-year Comparison Actual 2014 2015 2016 GDP

Economic Update Baker College - Flint Federal Reserve Bank of Chicago January 10, 2017 Paul Traub Senior Business Economist Main Economic Indicators Year-over-year Comparison Actual 2014 2015 2016 GDP

Integration of Economic and Construction Outlooks: A Case Study. Lorenz Kleist Consultant October 6, 2009

Integration of Economic and Construction Outlooks: A Case Study Lorenz Kleist Consultant October 6, 2009 The Client The European Rental Association (ERA) ERA is a young European association ERA represents

Integration of Economic and Construction Outlooks: A Case Study Lorenz Kleist Consultant October 6, 2009 The Client The European Rental Association (ERA) ERA is a young European association ERA represents

2013 North American Software Defined Data Center Management Platforms New Product Innovation Award

2013 North American Software Defined Data Center Management Platforms New Product Innovation Award 2013 New Product Innovation Award Software Defined Data Center Management Platforms North America, 2013

2013 North American Software Defined Data Center Management Platforms New Product Innovation Award 2013 New Product Innovation Award Software Defined Data Center Management Platforms North America, 2013

Systemic Analyser in Network Threats

Systemic Analyser in Network Threats www.project-saint.eu @saintprojecteu #saintprojecteu John M.A. Bothos jbothos@iit.demokritos.gr Integrated System Laboratory Institute of Informatics & Telecommunication

Systemic Analyser in Network Threats www.project-saint.eu @saintprojecteu #saintprojecteu John M.A. Bothos jbothos@iit.demokritos.gr Integrated System Laboratory Institute of Informatics & Telecommunication

IAB internet advertising revenue report 2017 first six-months results

www.pwc.com www.iab.net IAB internet advertising revenue report 2017 first six-months results PwC Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed

www.pwc.com www.iab.net IAB internet advertising revenue report 2017 first six-months results PwC Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed

IFC ENERGY STORAGE MARKET REPORT

IFC ENERGY STORAGE MARKET REPORT DEVELOPMENTS AND OPPORTUNITIES FOR ENERGY STORAGE IN EMERGING MARKETS JANUARY 9, 2016 ANISSA DEHAMNA PRINCIPAL RESEARCH ANALYST NAVIGANT RESEARCH 1 / 2016 NAVIGANT CONSULTING,

IFC ENERGY STORAGE MARKET REPORT DEVELOPMENTS AND OPPORTUNITIES FOR ENERGY STORAGE IN EMERGING MARKETS JANUARY 9, 2016 ANISSA DEHAMNA PRINCIPAL RESEARCH ANALYST NAVIGANT RESEARCH 1 / 2016 NAVIGANT CONSULTING,

Change & Configuration Management Market

Change & Configuration Management Market Table of Contents 1. Market Size & Forecast... 3 2. Geographic Segmentation... 4 2.1 Change & Configuration Management Market in Americas... 4 2.2 Americas - Market

Change & Configuration Management Market Table of Contents 1. Market Size & Forecast... 3 2. Geographic Segmentation... 4 2.1 Change & Configuration Management Market in Americas... 4 2.2 Americas - Market

Pay-TV services worldwide: trends and forecasts PAY-TV SERVICES WORLDWIDE: TRENDS AND FORECASTS

RESEARCH FORECAST REPORT PAY-TV SERVICES WORLDWIDE: TRENDS AND FORECASTS 2017 2022 MARTIN SCOTT and ROMAN ORVISKY Analysys Mason Limited 2018 About this report This report provides: forecasts for the number

RESEARCH FORECAST REPORT PAY-TV SERVICES WORLDWIDE: TRENDS AND FORECASTS 2017 2022 MARTIN SCOTT and ROMAN ORVISKY Analysys Mason Limited 2018 About this report This report provides: forecasts for the number

World RF Coax Connector Market

World RF Coax Connector Market Report No.: P 680 14 May 2014 World RF Coax Connector Market Bishop and Associates, Inc. has just released a new six chapter, 182 page research report providing a detailed

World RF Coax Connector Market Report No.: P 680 14 May 2014 World RF Coax Connector Market Bishop and Associates, Inc. has just released a new six chapter, 182 page research report providing a detailed

Mobile Phones, Poor Economy to Dampen PDA Market to 2007

Forecast Analysis Mobile Phones, Poor Economy to Dampen PDA Market to 2007 Abstract: A stagnant economy and growing competition from mobile phones have reduced our expectations for PDA market growth. Worldwide

Forecast Analysis Mobile Phones, Poor Economy to Dampen PDA Market to 2007 Abstract: A stagnant economy and growing competition from mobile phones have reduced our expectations for PDA market growth. Worldwide

The Next Generation of Mobile Learning. Tamar Elkeles, Qualcomm Kevin Oakes, i4cp

The Next Generation of Mobile Learning Tamar Elkeles, Qualcomm Kevin Oakes, i4cp About i4cp i4cp focuses on the people practices that make high performance organizations unique. High-performance organizations

The Next Generation of Mobile Learning Tamar Elkeles, Qualcomm Kevin Oakes, i4cp About i4cp i4cp focuses on the people practices that make high performance organizations unique. High-performance organizations

Q Results. Emirates Integrated Telecommunications Company PJSC May 2014

Q1 214 Results Emirates Integrated Telecommunications Company PJSC May 214 Disclaimer Emirates Integrated Telecommunications Company PJSC (hereafter du ) is a telecommunication services provider in the

Q1 214 Results Emirates Integrated Telecommunications Company PJSC May 214 Disclaimer Emirates Integrated Telecommunications Company PJSC (hereafter du ) is a telecommunication services provider in the

Midsize Business Voice Service Spending Steady for 2003

End-User Analysis Midsize Business Voice Service Spending Steady for 23 Abstract: Telecom service providers need to know the voice telecom spending plans of the margin-rich midsize business segment in

End-User Analysis Midsize Business Voice Service Spending Steady for 23 Abstract: Telecom service providers need to know the voice telecom spending plans of the margin-rich midsize business segment in

Information & Communication Technology Statistics 2017

Information & Communication Technology Statistics 2017 STATISTICS BOTSWANA Private Bag 0024 Gaborone Botswana Tel: (+267) 367 1300. Fax: (+267) 395 2201. Toll Free: 0800 600 200 Email: info@statsbots.org.bw

Information & Communication Technology Statistics 2017 STATISTICS BOTSWANA Private Bag 0024 Gaborone Botswana Tel: (+267) 367 1300. Fax: (+267) 395 2201. Toll Free: 0800 600 200 Email: info@statsbots.org.bw

Western European Consumer Digital Camera Forecast:

June 26, 2009 Abstract Western European Consumer Digital Camera Forecast: 2008-2014 Report Fast Facts Published: June 2009 Pages: 75 Tables & Figures: 53 Price: $4,770 Order Information To place your order

June 26, 2009 Abstract Western European Consumer Digital Camera Forecast: 2008-2014 Report Fast Facts Published: June 2009 Pages: 75 Tables & Figures: 53 Price: $4,770 Order Information To place your order

Federation of Tax Administrators Conference Minneapolis, Minnesota September 26, 2001

Federation of Tax Administrators Conference Minneapolis, Minnesota September 26, 2001 Measurement Framework Measurement Activities Overview н Present, Future & Unfunded Lessons Learned Opportunities to

Federation of Tax Administrators Conference Minneapolis, Minnesota September 26, 2001 Measurement Framework Measurement Activities Overview н Present, Future & Unfunded Lessons Learned Opportunities to

AVOIDING SILOED DATA AND SILOED DATA MANAGEMENT

AVOIDING SILOED DATA AND SILOED DATA MANAGEMENT Dalton Cervo Author, Consultant, Data Management Expert March 2016 This presentation contains extracts from books that are: Copyright 2011 John Wiley & Sons,

AVOIDING SILOED DATA AND SILOED DATA MANAGEMENT Dalton Cervo Author, Consultant, Data Management Expert March 2016 This presentation contains extracts from books that are: Copyright 2011 John Wiley & Sons,

2017 Inpatient Telemedicine Study

2017 Inpatient Telemedicine Study www.himssanalytics.com Enabling better health through information technology. Telemedicine Study Introduction The concept of telemedicine - meaning the transfer of medical

2017 Inpatient Telemedicine Study www.himssanalytics.com Enabling better health through information technology. Telemedicine Study Introduction The concept of telemedicine - meaning the transfer of medical

Kentucky IT Consolidation

2007 NASCIO Recognition Awards Nomination Category: Enterprise IT Management Initiatives Kentucky IT Consolidation Commonwealth Office of Technology The Commonwealth of Kentucky is nearing completion of

2007 NASCIO Recognition Awards Nomination Category: Enterprise IT Management Initiatives Kentucky IT Consolidation Commonwealth Office of Technology The Commonwealth of Kentucky is nearing completion of

Meaningful Use of Wearables Data

Meaningful Use of Wearables Data JESSICA GROSSMEIER, PHD, MPH HERO VICE PRESIDENT, R ESEARCH FEBRUA RY 9, 2016 ALL WORKPLACES POSITIVELY INFLUENCE THE HEALTH AND WELL-BEING OF EMPLOYEES, THEIR FAMILIES

Meaningful Use of Wearables Data JESSICA GROSSMEIER, PHD, MPH HERO VICE PRESIDENT, R ESEARCH FEBRUA RY 9, 2016 ALL WORKPLACES POSITIVELY INFLUENCE THE HEALTH AND WELL-BEING OF EMPLOYEES, THEIR FAMILIES

A Portrait of Today s Smartphone User

A Portrait of Today s Smartphone User August 2012 Conducted in partnership with www.online-publishers.org Frank N. Magid Associates, Inc. Who We Are: Frank N. Magid Associates, Inc. is a leading research-based

A Portrait of Today s Smartphone User August 2012 Conducted in partnership with www.online-publishers.org Frank N. Magid Associates, Inc. Who We Are: Frank N. Magid Associates, Inc. is a leading research-based

2016 Market Update. Gary Keller and Jay Papasan Keller Williams Realty, Inc.

2016 Market Update Gary Keller and Jay Papasan Housing Market Cycles 1. Home Sales The Numbers That Drive U.S. 2. Home Price 3. Months Supply of Inventory 4. Mortgage Rates Real Estate 1. Home Sales Nationally

2016 Market Update Gary Keller and Jay Papasan Housing Market Cycles 1. Home Sales The Numbers That Drive U.S. 2. Home Price 3. Months Supply of Inventory 4. Mortgage Rates Real Estate 1. Home Sales Nationally

Global Voice Recognition Market for Smartphones

Global Voice Recognition Market for Smartphones 2015-2019 Global Voice Recognition Market for Smartphones 2015-2019 Sector Publishing Intelligence Limited (SPi) has been marketing business and market research

Global Voice Recognition Market for Smartphones 2015-2019 Global Voice Recognition Market for Smartphones 2015-2019 Sector Publishing Intelligence Limited (SPi) has been marketing business and market research

MOBILE SERVICES IN THE MIDDLE EAST AND NORTH AFRICA: TRENDS AND FORECASTS

RESEARCH FORECAST REPORT MOBILE SERVICES IN THE MIDDLE EAST AND NORTH AFRICA: TRENDS AND FORECASTS 2017 2022 JULIA MARTUSEWICZ-KULINSKA Analysys Mason Limited 2017 analysysmason.com About this report This

RESEARCH FORECAST REPORT MOBILE SERVICES IN THE MIDDLE EAST AND NORTH AFRICA: TRENDS AND FORECASTS 2017 2022 JULIA MARTUSEWICZ-KULINSKA Analysys Mason Limited 2017 analysysmason.com About this report This

2013, Healthcare Intelligence Network

Note: This is an authorized excerpt from 2013 Healthcare Benchmarks: Mobile Health. To download the entire report, go to http://store.hin.com/product.asp?itemid=4586 or call 888-446-3530. 2013, Healthcare

Note: This is an authorized excerpt from 2013 Healthcare Benchmarks: Mobile Health. To download the entire report, go to http://store.hin.com/product.asp?itemid=4586 or call 888-446-3530. 2013, Healthcare

RightScale 2018 State of the Cloud Report DATA TO NAVIGATE YOUR MULTI-CLOUD STRATEGY

RightScale 2018 State of the Cloud Report DATA TO NAVIGATE YOUR MULTI-CLOUD STRATEGY RightScale 2018 State of the Cloud Report As Public and Private Cloud Grow, Organizations Focus on Governing Costs Executive

RightScale 2018 State of the Cloud Report DATA TO NAVIGATE YOUR MULTI-CLOUD STRATEGY RightScale 2018 State of the Cloud Report As Public and Private Cloud Grow, Organizations Focus on Governing Costs Executive

Global Elevator & Escalator Market: Industry Analysis & Outlook ( )

") Industry Research by Koncept Analytics Global Elevator & Escalator Market: Industry Analysis & Outlook ----------------------------------------- (2017-2021) July 2017 1 Executive Summary Elevator is a

Industry Research by Koncept Analytics Global Elevator & Escalator Market: Industry Analysis & Outlook ----------------------------------------- (2017-2021) July 2017 1 Executive Summary Elevator is a

Consistent Measurement of Broadband Availability

Consistent Measurement of Broadband Availability By Advanced Analytical Consulting Group, Inc. September 2016 Abstract This paper provides several, consistent measures of broadband availability from 2009

Consistent Measurement of Broadband Availability By Advanced Analytical Consulting Group, Inc. September 2016 Abstract This paper provides several, consistent measures of broadband availability from 2009

Securing Your Digital Transformation

Securing Your Digital Transformation Security Consulting Managed Security Leveraging experienced, senior experts to help define and communicate risk and security program strategy using real-world data,

Securing Your Digital Transformation Security Consulting Managed Security Leveraging experienced, senior experts to help define and communicate risk and security program strategy using real-world data,

Emerging Opportunities in Lebanon s Cards and Payments Industry

Emerging Opportunities in Lebanon s Cards and Payments Industry Industry Size, Trends, Factors, Strategies, Products and Competitive Landscape Product Code: VR0918MR Published Date: May 2013 www.timetric.com

Emerging Opportunities in Lebanon s Cards and Payments Industry Industry Size, Trends, Factors, Strategies, Products and Competitive Landscape Product Code: VR0918MR Published Date: May 2013 www.timetric.com

Acknowledgement: BYU-Idaho Economics Department Faculty (Principal authors: Rick Hirschi, Ryan Johnson, Allan Walburger and David Barrus)

") Math Review Acknowledgement: BYU-Idaho Economics Department Faculty (Principal authors: Rick Hirschi, Ryan Johnson, Allan Walburger and David Barrus) Section 1 - Graphing Data Graphs It is said that a

Math Review Acknowledgement: BYU-Idaho Economics Department Faculty (Principal authors: Rick Hirschi, Ryan Johnson, Allan Walburger and David Barrus) Section 1 - Graphing Data Graphs It is said that a

Mid-Market Data Center Purchasing Drivers, Priorities and Barriers

Mid-Market Data Center Purchasing Drivers, Priorities and Barriers Featuring Sophia Vargas, Forrester Research Inc. 30 May 2014 Introducing today s presenters: Matt Miszewski Senior Vice President of Sales

Mid-Market Data Center Purchasing Drivers, Priorities and Barriers Featuring Sophia Vargas, Forrester Research Inc. 30 May 2014 Introducing today s presenters: Matt Miszewski Senior Vice President of Sales

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook Illinois Public Pension Fund Association Hoffman Estates, IL February 16, 217 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago GDP expanded by 1.9%

Economic Outlook Illinois Public Pension Fund Association Hoffman Estates, IL February 16, 217 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago GDP expanded by 1.9%

Worldwide Hosted PBX Market Table of Contents. EasternManagementGroup 0

Worldwide Hosted PBX Market 2018-2024 Table of Contents EasternManagementGroup 0 2018 The Eastern Management Group, Inc. EasternManagementGroup 1 Introduction Worldwide Hosted PBX Market 2018-2024 was

Worldwide Hosted PBX Market 2018-2024 Table of Contents EasternManagementGroup 0 2018 The Eastern Management Group, Inc. EasternManagementGroup 1 Introduction Worldwide Hosted PBX Market 2018-2024 was

Consistent Measurement of Broadband Availability

Consistent Measurement of Broadband Availability FCC Data through 12/2015 By Advanced Analytical Consulting Group, Inc. December 2016 Abstract This paper provides several, consistent measures of broadband

Consistent Measurement of Broadband Availability FCC Data through 12/2015 By Advanced Analytical Consulting Group, Inc. December 2016 Abstract This paper provides several, consistent measures of broadband

Will 3G Networks Cope?

Brings together 3G traffic and capacity forecasts for the first time Unwired insight when a superficial assessment is not enough New report Will 3G Networks Cope? 3G traffic and capacity forecasts, 2009

Brings together 3G traffic and capacity forecasts for the first time Unwired insight when a superficial assessment is not enough New report Will 3G Networks Cope? 3G traffic and capacity forecasts, 2009

Chapter 3 Information and Communication Technology (ICT) and EEE Consumption Trends

and EEE Consumption Trends") Chapter 3 Information and Communication Technology (ICT) and EEE Consumption Trends The global information society is growing at great speed. More and faster networks, and new applications and services

Chapter 3 Information and Communication Technology (ICT) and EEE Consumption Trends The global information society is growing at great speed. More and faster networks, and new applications and services

LPWA NETWORKS FOR IoT: WORLDWIDE TRENDS AND FORECASTS

RESEARCH FORECAST REPORT LPWA NETWORKS FOR IoT: WORLDWIDE TRENDS AND FORECASTS 2015 2025 MICHELE MACKENZIE Analysys Mason Limited 2016 analysysmason.com About this report Low-power, wide-area (LPWA) is

RESEARCH FORECAST REPORT LPWA NETWORKS FOR IoT: WORLDWIDE TRENDS AND FORECASTS 2015 2025 MICHELE MACKENZIE Analysys Mason Limited 2016 analysysmason.com About this report Low-power, wide-area (LPWA) is

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook Midwest Association of Rail Shippers Lombard, IL January 13, 216 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The Great Recession ended in June

Economic Outlook Midwest Association of Rail Shippers Lombard, IL January 13, 216 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The Great Recession ended in June

Red Hat Acquisition of Qumranet Adds next generation virtualization capabilities. September 4, 2008

Red Hat Acquisition of Qumranet Adds next generation virtualization capabilities September 4, 2008 Safe Harbor Forward-Looking Statements Certain statements contained or discussed in this presentation

Red Hat Acquisition of Qumranet Adds next generation virtualization capabilities September 4, 2008 Safe Harbor Forward-Looking Statements Certain statements contained or discussed in this presentation

Bluetooth in Automotive Market Research Report - Global Forecast to 2023

Report Information More information from: https://www.marketresearchfuture.com/reports/1262 Bluetooth in Automotive Market Research Report - Global Forecast to 2023 Report / Search Code: MRFR/AM/0754-CRR

Report Information More information from: https://www.marketresearchfuture.com/reports/1262 Bluetooth in Automotive Market Research Report - Global Forecast to 2023 Report / Search Code: MRFR/AM/0754-CRR

Semiconductor Market for Data Processing: Asia/Pacific, 3Q03

Research Brief Semiconductor Market for Data Processing: Asia/Pacific, 3Q03 Abstract: Semiconductor market conditions have improved since the second quarter of 2003, and the industry's recovery is continuing.

Research Brief Semiconductor Market for Data Processing: Asia/Pacific, 3Q03 Abstract: Semiconductor market conditions have improved since the second quarter of 2003, and the industry's recovery is continuing.

Excerpt Costa Rica: Liberalization Will More Than Double Mobile Subscribers by 2015

Excerpt Costa Rica: Liberalization Will More Than Double Mobile Subscribers by 2015 This report is part of Pyramid Research s series of Latin America Country Intelligence Reports August 2010 Edition Jose

Excerpt Costa Rica: Liberalization Will More Than Double Mobile Subscribers by 2015 This report is part of Pyramid Research s series of Latin America Country Intelligence Reports August 2010 Edition Jose

EPS GROWTH MEASURES FOR INCENTIVE PAYMENTS WHAT ARE THEY REALLY REWARDING?

EPS GROWTH MEASURES FOR INCENTIVE PAYMENTS WHAT ARE THEY REALLY REWARDING? After relative Total Shareholder return (TSR) growth, Earnings Per Share (EPS) growth is the most common Long Term Incentive (LTI)

EPS GROWTH MEASURES FOR INCENTIVE PAYMENTS WHAT ARE THEY REALLY REWARDING? After relative Total Shareholder return (TSR) growth, Earnings Per Share (EPS) growth is the most common Long Term Incentive (LTI)

Digital SLRs and Other Interchangeable Lens Cameras: A Multi-Client Study

June 2010 Abstract Digital SLRs and Other Interchangeable Lens Cameras: A Multi-Client Study Report Fast Facts Published: June 2010 Pages: 114 Tables & Figures: 92 Price: $15,995 Order Information To place

June 2010 Abstract Digital SLRs and Other Interchangeable Lens Cameras: A Multi-Client Study Report Fast Facts Published: June 2010 Pages: 114 Tables & Figures: 92 Price: $15,995 Order Information To place

Segmented or Overlapping Dual Frame Samples in Telephone Surveys

Vol. 3, Issue 6, 2010 Segmented or Overlapping Dual Frame Samples in Telephone Surveys John M Boyle *, Faith Lewis, Brian Tefft * Institution: Abt SRBI Institution: Abt SRBI Institution: AAA Foundation

Vol. 3, Issue 6, 2010 Segmented or Overlapping Dual Frame Samples in Telephone Surveys John M Boyle *, Faith Lewis, Brian Tefft * Institution: Abt SRBI Institution: Abt SRBI Institution: AAA Foundation

Global Headquarters: 5 Speen Street Framingham, MA USA P F

WHITE PAPER SSDs: The Other Primary Storage Alternative Sponsored by: Samsung Jeff Janukowicz January 2008 Dave Reinsel IN THIS WHITE PAPER Global Headquarters: 5 Speen Street Framingham, MA 01701 USA

WHITE PAPER SSDs: The Other Primary Storage Alternative Sponsored by: Samsung Jeff Janukowicz January 2008 Dave Reinsel IN THIS WHITE PAPER Global Headquarters: 5 Speen Street Framingham, MA 01701 USA

Solid State Drives (SSD) Markets and Applications Quarterly Series: 1Q 2011

Markets and Applications Quarterly Series: 1Q 2011") Solid State Drives (SSD) Markets and Applications Quarterly Series: 1Q 2011 2010 2016 Report Number MS300SSD1-2011 Executive Summary This report is a series of four quarterly SSD reports focused on markets

Solid State Drives (SSD) Markets and Applications Quarterly Series: 1Q 2011 2010 2016 Report Number MS300SSD1-2011 Executive Summary This report is a series of four quarterly SSD reports focused on markets

Consensus Outlook

Consensus Outlook - 219 Thirty-second Annual Economic Outlook Symposium November 3, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The views expressed herein

Consensus Outlook - 219 Thirty-second Annual Economic Outlook Symposium November 3, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The views expressed herein

Telecom Cloud Market Research Report- Global Forecast 2022

Report Information More information from: https://www.marketresearchfuture.com/reports/2027 Telecom Cloud Market Research Report- Global Forecast 2022 Report / Search Code: MRFR/ICT/1495-HCRR Publish Date:

Report Information More information from: https://www.marketresearchfuture.com/reports/2027 Telecom Cloud Market Research Report- Global Forecast 2022 Report / Search Code: MRFR/ICT/1495-HCRR Publish Date:

Emerging Asia Pacific telecoms market: trends and forecasts EMERGING ASIA PACIFIC TELECOMS MARKET: TRENDS AND FORECASTS

REGIONAL FORECAST REPORT EMERGING ASIA PACIFIC TELECOMS MARKET: TRENDS AND FORECASTS 2017 2022 SHERRIE HUANG and CAI SHIYU About this report This report provides: a 5-year forecast of more than 180 mobile

REGIONAL FORECAST REPORT EMERGING ASIA PACIFIC TELECOMS MARKET: TRENDS AND FORECASTS 2017 2022 SHERRIE HUANG and CAI SHIYU About this report This report provides: a 5-year forecast of more than 180 mobile

Global Headquarters: 5 Speen Street Framingham, MA USA P F

Global Headquarters: 5 Speen Street Framingham, MA 01701 USA P.508.872.8200 F.508.935.4015 www.idc.com C O M P E T I T I V E A N A L Y S I S I D C M a r k e t S c a p e : W o r l d w i d e D a t a c e

Global Headquarters: 5 Speen Street Framingham, MA 01701 USA P.508.872.8200 F.508.935.4015 www.idc.com C O M P E T I T I V E A N A L Y S I S I D C M a r k e t S c a p e : W o r l d w i d e D a t a c e

Life Science Leading Indicators 2010 (July - December)

") Life Science Leading Indicators 2010 (July - December) Eric Newmark, Research Manager July 20, 2010 Methodology Health Industry Insights' Leading Indicators in Life Science IT Spending Survey is a bi-annual

Life Science Leading Indicators 2010 (July - December) Eric Newmark, Research Manager July 20, 2010 Methodology Health Industry Insights' Leading Indicators in Life Science IT Spending Survey is a bi-annual

M2M device connections and revenue: worldwide forecast

Research Forecast Report M2M device connections and revenue: worldwide forecast 2013 2023 August 2013 Morgan Mullooly and Steve Hilton 2 Contents Slide no. 5. About this report 6. Executive summary 7.

Research Forecast Report M2M device connections and revenue: worldwide forecast 2013 2023 August 2013 Morgan Mullooly and Steve Hilton 2 Contents Slide no. 5. About this report 6. Executive summary 7.

Cincinnati Bell Inc. March 4, 2013

Cincinnati Bell Inc. March 4, 2013 Safe Harbor This presentation and the documents incorporated by reference herein contain forwardlooking statements regarding future events and our future results that

Cincinnati Bell Inc. March 4, 2013 Safe Harbor This presentation and the documents incorporated by reference herein contain forwardlooking statements regarding future events and our future results that

Nigerian Telecommunications (Services) Sector Report Q2 2016

Sector Report Q2 2016") Nigerian Telecommunications (Services) Sector Report Q2 2016 01 SEPTEMBER 2016 Telecommunications Data The telecommunications data used in this report were obtained from the National Bureau of Statistics

Nigerian Telecommunications (Services) Sector Report Q2 2016 01 SEPTEMBER 2016 Telecommunications Data The telecommunications data used in this report were obtained from the National Bureau of Statistics

GDPR: A QUICK OVERVIEW

GDPR: A QUICK OVERVIEW 2018 Get ready now. 29 June 2017 Presenters Charles Barley Director, Risk Advisory Services Charles Barley, Jr. is responsible for the delivery of governance, risk and compliance

GDPR: A QUICK OVERVIEW 2018 Get ready now. 29 June 2017 Presenters Charles Barley Director, Risk Advisory Services Charles Barley, Jr. is responsible for the delivery of governance, risk and compliance

Global In-Vitro Diagnostics (IVD) Market: Industry Analysis & Outlook ( )

Market: Industry Analysis & Outlook ( )") Industry Research by Koncept Analytics Global In-Vitro Diagnostics (IVD) Market: Industry Analysis & Outlook ----------------------------------------- (2017-2021) October 2017 1 Executive Summary Diagnosis

Industry Research by Koncept Analytics Global In-Vitro Diagnostics (IVD) Market: Industry Analysis & Outlook ----------------------------------------- (2017-2021) October 2017 1 Executive Summary Diagnosis

Current and Next-Generation Switching in Asia/Pacific and Japan, 2003 (Executive Summary) Executive Summary